Content

Content

Public administration

8.1. Institutional structure

Service delivery responsibilities

- The public administration sector is a broad category that includes central and local government administration buildings and associated infrastructure. Public administration infrastructure underpins the functioning of democratic governance (Parliament and council chambers), while other central government buildings provide amenities and are considered elsewhere.

- Individual central government departments are responsible for procuring their own administration buildings, with centralised support from the Government Property Office (GPO). Apart from specialised and security focused assets, these are largely leased. For local government, this is the responsibility of councils, to the extent they own the buildings they use (as opposed to leasing office space) and the community assets they provide. While leasing buildings is an operating expense, the fit-out of the interiors is the responsibility of the tenant departments and can be a significant capital expense. This also provides for a separation of the repairs and maintenance responsibilities between the landlord for the building (for example, lifts) and the tenant for fittings.

Governance and oversight

- The Chief Executive of the Ministry of Business, Innovation and Employment (MBIE) is the System Lead for Property, and the GPO serves as their operational arm within MBIE. The GPO oversees around 940,000 square metres of property, including office accommodation and public interface areas, across roughly 70 central government organisations. Acting as the strategic coordinator for the central government property system, the GPO sets standards, provides tools and guidance, and approves all leasing activity to ensure effective property management.

- The GPO also administers and mandates the Government Property Portal (GPP), which agencies are required to submit their office accommodation data into. The GPO also assists with leasing and offers internal brokerage services to optimise the use of underutilised or vacant office space within the system.

- Public administration assets are distributed over central government departments and Crown agencies. Relevant ministries are responsible for policy and planning. Oversight tends to operate via budget and performance targets set by Ministerial expectations to improve productivity and cost efficiencies.

- The Department of Internal Affairs has an ongoing oversight function around the performance of the local government sector, which includes how it invests in and manages assets.

8.2. Paying for investment

- Funding of central government administration buildings and facilities comes from general taxation. Many central government office buildings are leased, but the leasing departments and agencies are responsible for the internal fit-out of the office space, and the associated maintenance and renewals for internal fittings.

- Funding for local government administration buildings is funded through rates.

8.3. Historical investment drivers

- Demand for office space would closely align with the movements in the size of the public sector, following the ebb and flow of headcount expansion and contraction.

- Public administration buildings will have relatively standardised renewal and maintenance requirements to maintain safety and capability to be occupied. They may also require investment to become more resilient to natural hazard events or to bring them up to modern standards.

8.4. Community perceptions and expectations

This section summarises what we know about the New Zealand public’s perceptions and expectations of the public administration sector, at a national level.

- We do not have data on New Zealander’s views on the quality of public administration buildings, but a recent 2022 survey found that around two-thirds of New Zealanders were satisfied with administrative services (68%), which is slightly above the OECD average (63%).200

8.5. Current state of network

- Stats NZ capital stock data is grouped into a large category of public administration and safety, which includes government buildings, corrections, justice, police, defence assets, and fire services. We have gathered data from entities’ annual reports to understand the scale of these subsectors.

- Initial analysis by the Commission indicates that the value of central government buildings and equipment not related to health, schools, justice, defence, or corrections to be around $12 billion in 2022.

- We estimate that since 2007, investment in these buildings was over $1 billion a year, on average.

- We don’t have full information on building condition, but we can observe the extent to which total investment (including renewals as well as improvements) is keeping up with depreciation. (Note: If investment falls below depreciation, this implies assets are being ‘sweated out’. However, even if investment is above depreciation, if that investment is directed to new infrastructure, it is still possible that existing assets are deteriorating at the expense of new infrastructure. In the absence of knowing renewal investment to depreciation specifically, the higher the ratio the better the overall condition of the asset base.)

- For overall public administration and safety, investment to depreciation ratios have averaged just over 150% since the year 2000. However, corrections investment has been elevated during the period, suggesting that the condition of central government buildings (and other subsectors of the category) has either been steady or declining (rather than improving) over the last 25 years.

8.6. Forward Guidance for capital investment demand

Forecast investment levels for central government administration buildings (excl. health and education)

This table provides further detail on our Forward Guidance, which is summarised in Chapter 3. Further information on this analysis and the underlying modelling assumptions is provided in a supporting technical report.201

- Our outlook for this sector is largely stable, with investment levels settling at close to the long-term trend. It is not expected that income and population dynamics will have a significant impact on the demand for central government buildings. This means that renewals and maintenance of the existing stock will be the primary driver of investment need.

8.7. Current investment intentions

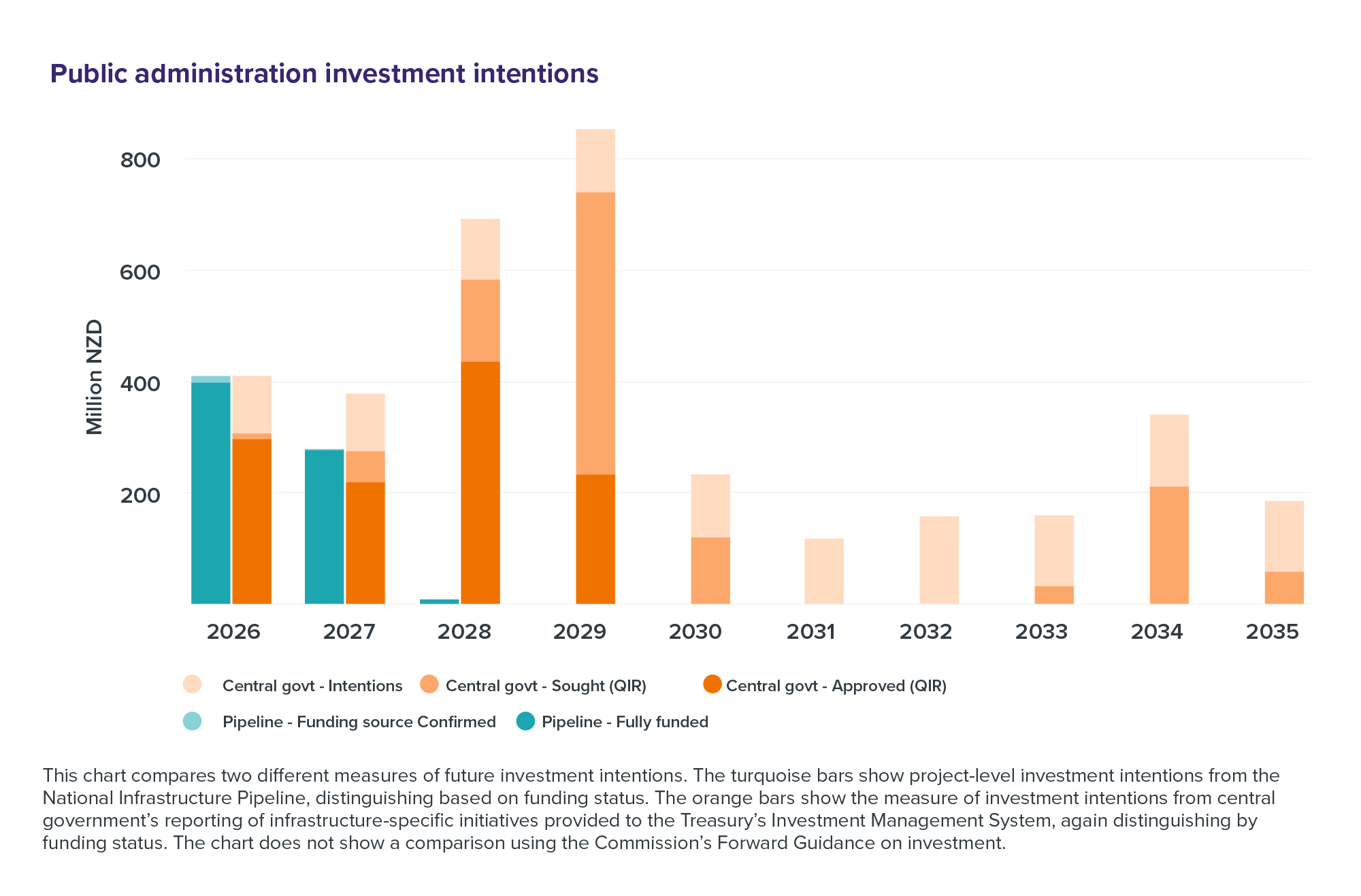

- For central government public administration buildings, our Forward Guidance for this sector is largely a multi-year indicative projection, rather than an annual target. As such, we have excluded it from the chart below.

- The following chart shows projected spending to deliver initiatives in planning and delivery in the Pipeline (turquoise bars) and programme-level intentions in central government’s reporting to the Treasury’s Investment Management System (orange bars) over the 2026–2035 period. Local government public administration buildings have not been included.

- Investment intentions and funding sought outweighs approved and funded projects.

Figure 53: Public administration investment intentions

This chart compares two different measures of future investment intentions. The turquoise bars show project-level investment intentions from the National Infrastructure Pipeline, distinguishing based on funding status. The orange bars show the measure of investment intentions from central government’s reporting of infrastructure-specific initiatives provided to the Treasury’s Investment Management System, again distinguishing by funding status. The chart does not show a comparison using the Commission’s Forward Guidance on investment.

{kind=link}

8.8. Key issues and opportunities

- Asset management: According to the Commission’s report ‘Taking care of tomorrow today: Asset management state of play’, development of long-term asset management and investment plans is a key opportunity for the sector. Better asset management will also give visibility about the scale and quality of the assets we have in this sector.

- Transparency and accountability: Central government, which has funding and oversight roles in this sector, has an opportunity to provide more transparency around its maintenance and renewal requirements.

- Project appraisal and evaluation: The evaluation of project proposals could be improved. Process improvements could include more effective cost estimation, optimising investments and understanding the prioritisation and trade-offs associated with investment decisions.

- Lease versus ownership: For general-purpose infrastructure such as office space, leasing is often preferred over ownership. Ownership exposes agencies to the risk that demand may fall below owned supply, leaving surplus space and sunk costs. Leasing a piece of infrastructure shifts that risk to the third party, who can reduce this risk by leasing to multiple tenants. This approach is standard for central government office accommodation, with the GPO actively seeking to move towards a more coordinated model that could unlock and maximise the benefits and efficiencies under this approach. There may be opportunities to shift to leasing for other general-purpose infrastructure or in the local government sector.