Content

Content

Ports

12.1. Institutional structure

Service delivery responsibilities

- There are thirteen major commercial ports in New Zealand: nine are in the North Island, all except Port Taranaki are on the east coast, and four are distributed mostly on the east coast of the South Island. Most ports are capable of handling containerised freight as well as commodities, like logs, and break-bulk cargo, and have specialised facilities to transit commodities with specific handling and storage requirements such as cement and fuel.

- In addition to the main commercial ports, New Zealand has numerous smaller commercial wharves that primarily serve specific industries such as fishing, coastal shipping, inter-island ferries, and local cargo or passenger needs. These wharves are typically managed by local councils, port companies, or private operators and are not included in the main international port statistics. These wharves also play an important role for shipping services to remote locations that include Stewart Island, the Chatham Islands and Great Barrier Island.

- Inland ports, also referred to as intermodal freight hubs, are an expanding component in the logistics network. They are a direct response to landside constraints faced by major seaports, such as Auckland and Tauranga. These strategically located facilities act as inland extensions of seaports, handling transfer of cargo between road and rail, and providing customs and biosecurity services.

- Most port companies are incorporated under the Port Companies Act 1988. They own and manage the physical port infrastructure (wharves, cranes) and provide services to shipping lines and cargo owners. There are a range of port ownership structures within the New Zealand port sector. Some ports are majority-owned by local/regional councils, while others have part private ownership and a listing on the New Zealand Stock Exchange, such as Port of Tauranga. There is also some cross-ownership between ports (for example, Port of Tauranga owns part of Northport and PrimePort Timaru).

Governance and oversight

- The Port Companies Act 1988 corporatised the former harbour boards and has shaped the current structure of the sector. The Maritime Transport Act 1994 (safety, security and environmental protection), Local Government Act 2002 (commercial relationship between local councils and their port entities), Resource Management Act 1991 (planning and consenting process and environmental protection for coastal areas) provide the suite of legislative governance.

- The Minister of Transport is responsible for overall transport policy, including the maritime and port sectors, appoints the board of Maritime NZ and can issue high-level policy direction. The Ministry of Transport advises the Minister on the legislative framework, funding, and governance of transport Crown entities like Maritime NZ. The Commerce Commission enforces the Commerce Act by monitoring for anti-competitive behaviour but does not regulate the port sector under Section 4 of the Act like it does for specified airports.

- Maritime NZ, in partnership with port operators and regional councils, develops and maintains the New Zealand Port and Harbour Marine Safety Code. This voluntary code is an institutional arrangement that translates the high-level safety duties of the Maritime Transport Act into specific, good-practice operational standards for managing navigation and safety within ports.

- Regional councils translate the Resource Management Act into regional plans that specify environmental standards and consent requirements for costal port activities. Regional councils are also delegated the Harbourmaster function, which retains the authority, legal responsibility and enforcement powers for maritime safety in the harbour jurisdiction.

12.2. Paying for investment

- Capital investment by maritime ports is primarily funded by the port companies themselves through retained earnings and debt. For significant investments, some council-owned ports have undertaken partial privatisation by listing on the NZX to raise capital. These costs are expected to be recouped through charges on port users.

- Port companies also often develop inland ports, sometimes in partnership with other entities. For example, the Ruakura inland port just outside of Hamilton is a joint venture between Port of Tauranga and Tainui, with KiwiRail as the main transport provider.

- Central government occasionally provides targeted funding for specific projects, often aimed at enhancing regional development, resilience, or connectivity.

12.3. Historical investment drivers

- During its early development, New Zealand relied heavily on ports and coastal shipping to service the isolated communities dispersed around the country. This has given the country its existing pattern of ports and commercial wharves.

- Dependence on regional ports has reduced over time through internal competition as land transport alternatives gained traction. Technological change in shipping through containerisation and logistics management changed the requirements from the 1970s onwards around wharf design and configuration, while increases in ship size reduced ship calls and consolidated port activity.

- Integration and coordination with land transport networks has become increasingly important over time, which has seen increases in shared use of road and rail infrastructure. This is linked to the increasing use of inland port facilities and just in time cargo arrival or clearance.

12.4. Community perceptions and expectations

- The Commission does not have any specific information about whether ports are meeting community expectations or needs.

- The Ministry of Transport publishes measures of port container productivity that give insights into how well ports are meeting consumer expectations.212.Productivity levels peaked around 2017 and fell sharply in 2021 due to COVID-19 related disruptions. Productivity increased somewhat in 2024 but it remains significantly below 2017 levels. This productivity trend is broadly consistent with international trends, with global measures of container port performance falling significantly in 2021 and as of 2024 remain at low levels. New Zealand and Australia have consistently lower port productivity levels than in many other regions.213

- Parliament’s Transport and Infrastructure Select Committee is conducting an inquiry into ports and the maritime sector. Submissions to the Committee, including from international shipping lines, note an expectation that the sector will need to improve productivity and coordination to adapt to the amalgamation and rationalisation of international shipping services.

- Port use of urban waterfront space often leads to trade-offs between port operations and use of waterfront for public and commercial purposes. This is most clearly seen in Auckland with proposals to reduce the footprint of the port, or move it entirely, to allow for other uses of Auckland waterfront space.

12.5. Current state of network

- The total fixed capital stock (excluding land) of New Zealand’s seven busiest ports was over $3.3 billion total in 2024.214

- Capital investment in the seven busiest ports averaged a total of $235 million per year between 2020 and 2024.

- We don’t have full information on building condition, but we can observe the extent to which total investment (including renewals as well as improvements) is keeping up with depreciation.(Note: If investment falls below depreciation, this implies assets are being ‘sweated out’. However, even if investment is above depreciation, if that investment is directed to new infrastructure, it is still possible that existing assets are deteriorating at the expense of new infrastructure. In the absence of knowing renewal investment to depreciation specifically, the higher the ratio the better the overall condition of the asset base.) Investment to depreciation ratios for the seven busiest ports averaged 207% between 2020 and 2024.

12.6. Forward Guidance for capital investment

- The Commission does not produce Forward Guidance forecasts for investment in ports infrastructure.

- We expect that at a high level, future demand for ports will be a function of economic dynamics in New Zealand, but also abroad. These dynamics reflect the changing structure and composition of the New Zealand economy, including which sectors continue to be sources of growth and generators of merchandise trade. Changes to the container trade, including the use of larger ships and potentially fewer port calls, along with changes to shipping routes following geopolitical events, will also shape port infrastructure investment.

12.7. Current investment intentions

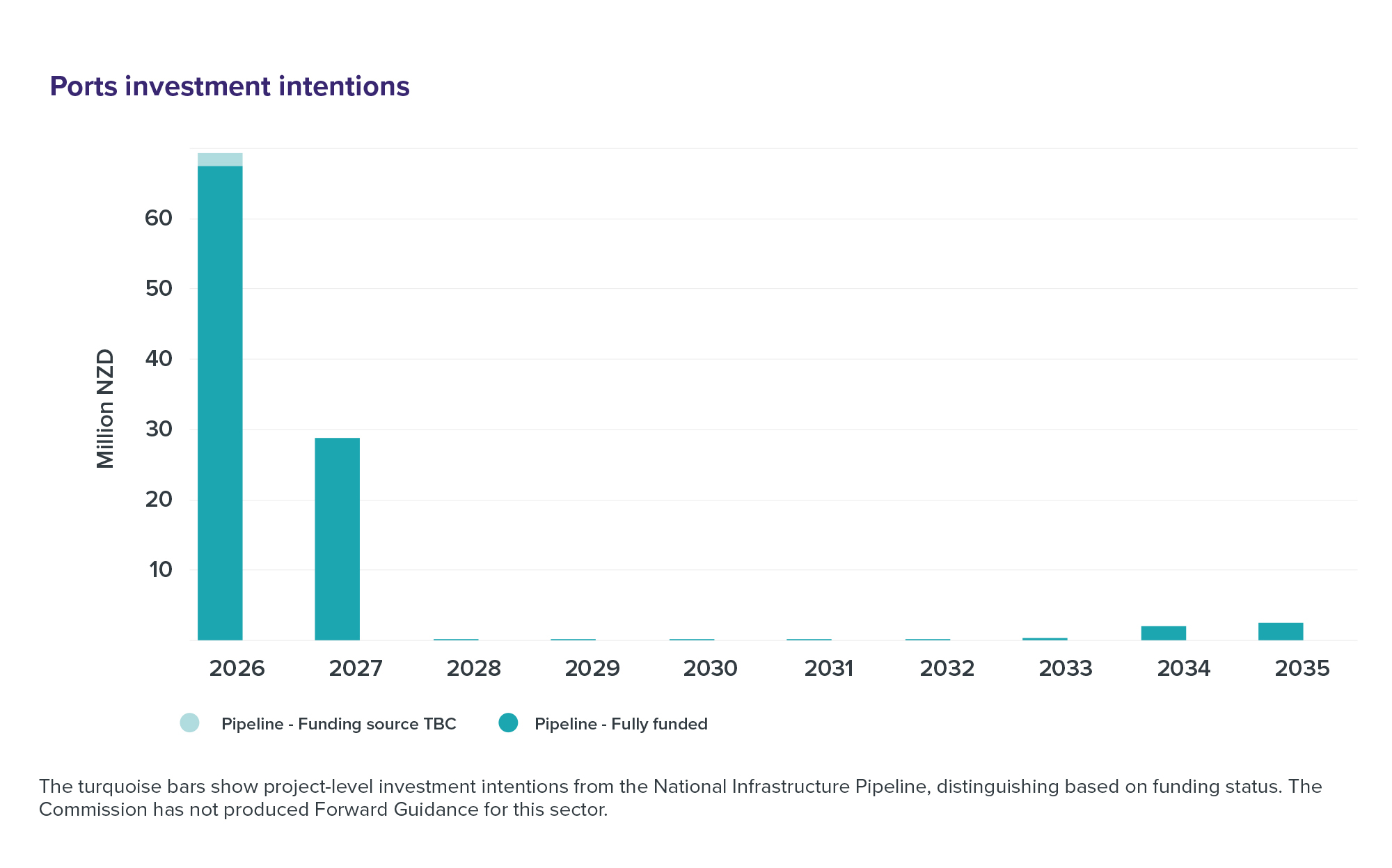

- The Pipeline currently collects only a limited amount of data from port companies or council-owned operations and appears to show primarily fully funded projects.

Figure 57: Ports investment intentions

The turquoise bars show project-level investment intentions from the National Infrastructure Pipeline, distinguishing based on funding status. The Commission has not produced Forward Guidance for this sector.

{kind=link}

12.8. Key issues and opportunities

- National coordination: A key challenge identified by the sector has been fragmented decision-making and competition between regionally owned ports. NZTA’s Action Plan for Freight is an opportunity to improve coordination in the sector.

- Shipping services: The ongoing amalgamation and rationalisation of international shipping services presents strategic challenges for the sector, including the impacts of managing fewer ship visits by agglomerating cargoes and the adoption of hub and spoke models for freight distribution, where a central location (‘hub’) consolidates and routes cargo to and from peripheral destinations. The trend to larger ships also places pressure on ports to manage calls from these ships, including infrastructure demands (deeper channels, larger berths, crane capability and landside capacity), and to manage more noticeable cargo peaks.

- Competing land use and accessibility: Population growth in our city centres is leading to more demand for waterfront space, which can compete for space against port infrastructure. The Port of Auckland is an example of where both rail and road access are constraints that possibly offset any wharf expansion. Decommissioning a port within an urban centre and establishing or expanding a new one would be a significant investment, and would need large, concrete benefits to justify the investment. However, where this has worked best overseas, such as the closure of Manhattan’s wharf in favour of Port Newark, or the development of Port Botany in Sydney, new ports have been close by to the facilities they have replaced.