Content

Content

Airports

13.1. Institutional structure

Service delivery responsibilities

- Scheduled air services operate out of 26 airports across the country. Six of these airports (Auckland, Christchurch, Queenstown, Wellington, Dunedin and Hamilton) currently host international air services.

- The remaining 20 airports form a regional network that provides domestic connectivity, including access to the main international hubs, economic (for example, tourism, freight) and social connectivity, as well as access to emergency and medical services.

- Beneath the main airports there are a range of licensed aerodromes (around 102, including the main airports) and airstrips that are either council or privately owned. These allow for recreational flying, flight training, agricultural aviation, air ambulance services and provide access to remote locations.

Governance and oversight

- The sector is covered by the Civil Aviation Act 2023, which provides the overarching framework for aviation security, safety, operations and sector regulation. The Airport Authorities Act 1966 grants powers to airport operators and the Commerce Act 1986 governs economic regulation, with major airports (Auckland, Christchurch and Wellington) subject to information disclosure regulations under Part 4.

- The ownership structures of the main international and regional airports vary. Auckland (AIAL) is an NZX listed entity, Wellington is majority owned by a listed infrastructure company (Infratil), while Christchurch is majority owned by Christchurch City Council, with the Crown holding a minority stake. Most remaining regional airports are structured either through direct council ownership and management or are operated through council-controlled organisations (CCOs), while a small number are Crown-Council joint ventures (for example, Taupō) or are privately owned.

- The Ministry of Transport is the primary central government agency responsible for policy and legislation for the aviation sector. It oversees the Crown's interest in joint-venture airports, as well as providing monitoring and oversight of Crown agencies operating in the sector, including the Civil Aviation Authority (CAA) and Airways New Zealand. MBIE is involved in competition policy and the economic regulation of airports.

- Sector oversight is achieved through the Civil Aviation Authority and its subsidiary Aviation Security (AvSec), which is responsible for safety and security regulation, setting the rules governing civil aviation and certification. Airways New Zealand operates as a state-owned enterprise and is the monopoly provider of air navigation and air traffic control systems and services. The Commerce Commission oversees the information disclosure regime for the three largest airports in the country (Auckland, Christchurch and Wellington).

13.2. Paying for investment

- Part 7 of the Civil Aviation Act 2023 requires that airports be operated on a commercial basis, with exceptions made for airports operated by local authorities or those owned and operated as CCOs. This means the key funding approach is based around a user-pays principle for infrastructure access and operations. Airport landing charges are not directly regulated, but large airports are required to consult with customers, like airlines, on major capital plans before setting charges.

- Major international airports are largely self-funding through aeronautical and non-aeronautical revenue, debt, and equity. The ability to generate non-aeronautical revenue, such as property development and retail operations, provides an additional funding source for airport development.

- Regional airports often rely on a mix of commercial (aeronautical and non-aeronautical) revenue, local government funding, and central government grants (e.g. Provincial Growth Fund, Regional Infrastructure Fund). Some smaller airports struggle with financial sustainability due to low usage and the requirement to maintain their assets to high standards.

- Occasional central government funding for regional airports helps to maintain essential infrastructure that enables connectivity for smaller communities.

13.3. Historical investment drivers

- Following the Second World War, a strong national development effort through the establishment of the National Airways Corporation to develop main trunk and feeder routes, drove the expansion of airport infrastructure and airline services to create the loosely affiliated network of airports that are present to this day.

- A more recent phenomenon that has driven both international and regional airport investment has been the growth of New Zealand as an international destination for tourists. This has necessitated ongoing investment in terminal capacities, airside infrastructure (runways and aprons) and facilities for customs processing and biosecurity. The growth in international flights has also required further investment in airport and aviation operating systems and equipment, such as air traffic control, radar, runway lighting and instrument landing systems.

- Changes in airline fleet composition have also had a material impact on airport investment. The introduction of larger aircraft, through the transition from propeller to jet engine, has driven investment in runway lengthening and widening and the hardening of aprons, as well as the requirement for upgraded terminal gates to accommodate the new aircraft.

- The move to airport corporatisation and the focus on commercial models for airport funding has moved airport investment into facilities that generate both aeronautical and non-aeronautical revenues, particularly through commercial development of landside properties like hotels.

13.4. Community perceptions and expectations

- Overall, it appears airport infrastructure is meeting New Zealanders’ needs.

- One study showed that 81% of New Zealanders rate the quality of New Zealand’s airports as very or fairly good, higher than a global average of 72%, and few (15%) identified airports as an area of priority for further investment.215

13.5. Current state of network

- New Zealand’s three largest international airports (Auckland, Wellington, and Christchurch) had a fixed-asset stock (excluding land) of nearly $6.4 billion in 2024.

- The value of the capital stock has increased rapidly over the past 10 years, with investment averaging nearly $460 million between 2017 and 2024 across the three airports. Investment in 2024 alone was over $1 billion, $992 million of this being in Auckland Airport.

- We don’t have full information on building conditions, but we can observe the extent to which total investment (including renewals as well as improvements) is keeping up with depreciation.(Note: If investment falls below depreciation, this implies assets are being ‘sweated out’. However, even if investment is above depreciation, if that investment is directed to new infrastructure, it is still possible that existing assets are deteriorating at the expense of new infrastructure. In the absence of knowing renewal investment to depreciation specifically, the higher the ratio the better the overall condition of the asset base.) Investment to depreciation ratios for New Zealand’s three largest airports averaged nearly 250% between 2016 and 2024.

13.6. Forward Guidance for capital investment

- The Commission does not produce Forward Guidance forecasts for airport infrastructure investment.

- Air travel, and therefore demand for infrastructure, has been found to be more sensitive to income than other infrastructure, with international air travel being more driven by income growth than domestic travel. This suggests that slower income growth driven by demographic dynamics and productivity into the future may be a headwind for air travel. Policy targets for international visitor arrivals are for 5 million arrivals by 2030 under the Government’s Tourism Growth Roadmap, which, if met, will place additional demands on the airport system, along with the connectivity to the land transport system.

- Decarbonising our economy could be a driver of future investment, as aviation transitions to low-carbon travel. This includes planning for the infrastructure required to support new, lower-emission aircraft technologies (for example, electric, hydrogen) and reducing ground-based emissions. Any such moves would place additional requirements on other infrastructure sectors, such as electricity generation and distribution.

- Improving system resilience could also be an important future investment area for airports which can be utilised as support lifelines during emergencies.

13.7. Current investment intentions

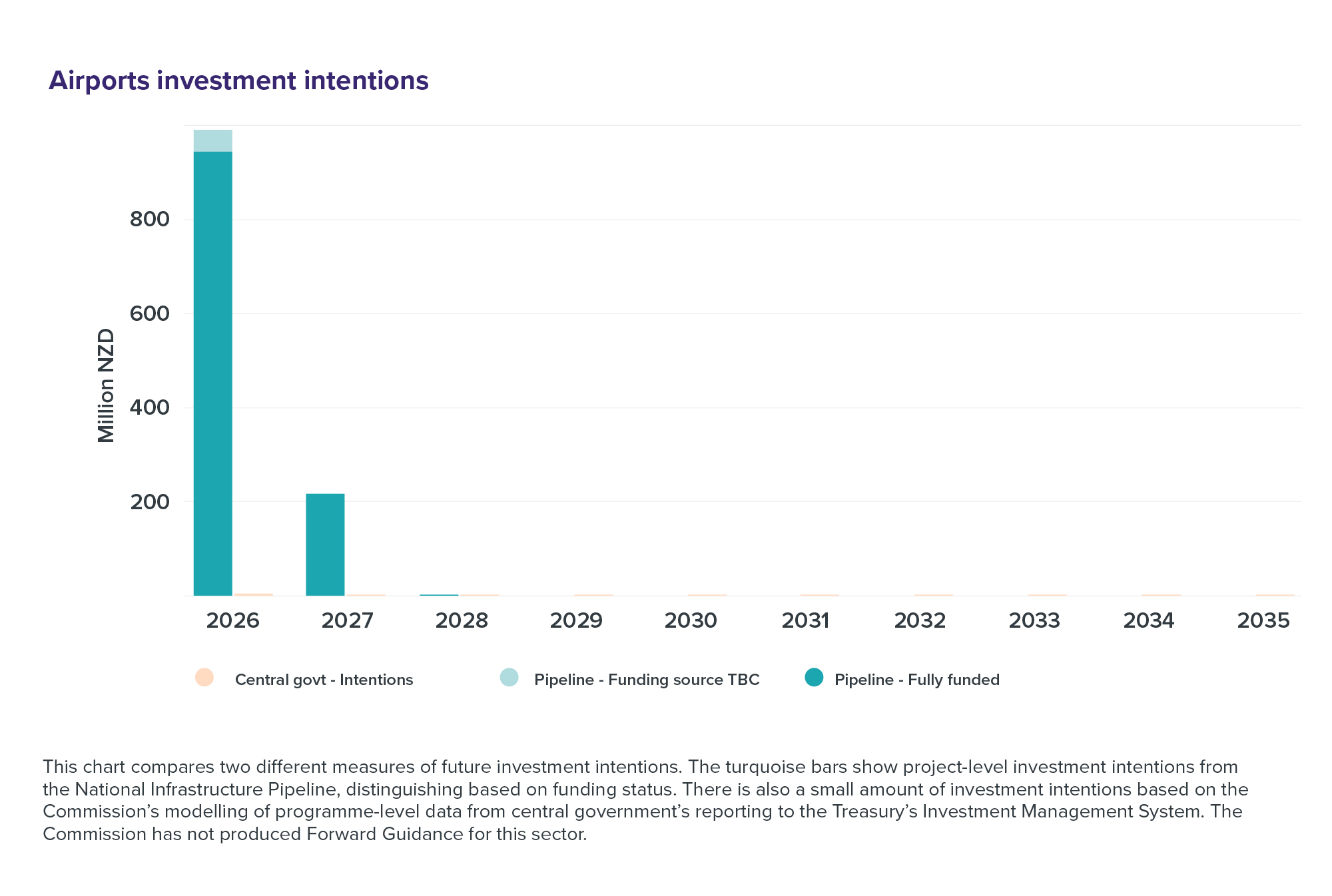

- The Pipeline currently collects only a limited amount of data from airport companies and council-owned operations which are primarily fully funded.

- Central government investment intentions are limited to investments proposed for joint-venture airports.

Figure 58: Airports investment intentions

This chart compares two different measures of future investment intentions. The turquoise bars show project-level investment intentions from the National Infrastructure Pipeline, distinguishing based on funding status. There is also a small amount of investment intentions based on the Commission’s modelling of programme-level data from central government’s reporting to the Treasury’s Investment Management System. The Commission has not produced Forward Guidance for this sector.

{kind=link}

13.8. Key issues and opportunities

- Funding and affordability: Large renewal investments in core infrastructure could strain affordability, particularly for regional airports with lower passenger numbers. The cost and scale of capital programmes highlight the difficulties with applying the user-pays model to recover costs from a relatively small base of users, in this case, airlines, who then pass costs on to consumers.

- Governance and ownership models: Central and local government support for airports is provided in part through direct ownership. This can lead to issues when airports are smaller, and either are not very profitable or do not make enough revenue to fully cover their costs. Central and local government face significant capital investment demands in other areas, raising the question of whether investments in airports should be recycled to fund higher priority investments.

- Decarbonisation: The transition towards decarbonisation and low-emission aviation presents a major challenge, that will likely require a substantial commitment to long-term investment in new infrastructure and the development and management of new energy sources. This is currently playing out in a highly uncertain technological environment.

- Technological change: New technologies like artificial intelligence and data analytics for ground operations and terminal configuration offers an opportunity to improve the efficiency of existing assets, optimise resource allocation, and provide a more seamless and predictable journey for passengers. Currently Auckland, Christchurch and Queenstown are experimenting with new technologies, while the CAA is looking to streamline security screening.216The challenge will be rolling out technical changes to smaller undercapitalised regional airports.