Content

Content

Gas

4.1. Institutional structure

Service delivery responsibilities

- This sector summary focuses on ‘downstream’ gas transmission, distribution and retail. It excludes liquid fuels (for example, petrol and diesel) and ‘upstream’ gas production and processing activities. While the focus is on the transmission and distribution networks, these rely upon the presence of ongoing volumes of gas in sufficient quantities to make the operation of these networks viable.

- Gas infrastructure and services are provided by non-government entities. Gas transmission is provided by Firstgas (part of Clarus Group, which is in the process of being acquired by Brookfield), which owns and operates the high-pressure gas transport pipelines. Distribution through low-pressure networks to end users is provided by Firstgas, Vector, Powerco, Nova and GasNet (a council-owned provider in the Manawatū-Whanganui area). Transmission and distribution companies operate as regulated monopolies. There are several gas retail companies, such as Nova Energy, Contact Energy and Genesis Energy, which buy gas wholesale to sell to businesses and households. Distributed gas is only available in the North Island, with bottled LPG available for South Island consumers.

- Gas delivery works on a series of contracts across the production and network components of the sector. Gas is generally wholesaled through Gas Supply Agreements (GSAs), which are long-term bilateral contracts between producers and large users or retailers. The spot market comprises just under 5% of gas production.177 The long-term contracts specify volume, price, delivery points, and duration. Large users and retailers then have transmission and distribution agreements with pipeline operators to transport gas for a pre-determined (regulated) tariff. Only 4% of natural gas is consumed by households,178 but they comprise over 90% of connections.

Governance and oversight

- The Gas Act 1992 provides for sector legislation around safety standards, a co-regulatory governance model and the establishment of the Gas Industry Company (GIC). The Commerce Act 1986 empowers the Commerce Commission under Part 4 of the Act to regulate gas networks, under the current (2023) default price-quality path that has been in place since October 2022. A new (2026) path is currently under development for commencement on 1 October 2026.

- The ‘downstream’ gas sector is governed by regulations developed by the government and the GIC. The GIC is a form of industry self-regulation governed by the largest industry players, which makes recommendations to the Minister for Energy on rules and regulations.

- MBIE provides policy stewardship for both gas and electricity because of the interdependencies between them. Gas remains complementary to electricity generation, with around 9% of electricity generated using gas in 2023.

4.2. Paying for investment

- Investment in gas transmission and distribution infrastructure is privately funded by the network owners (for example, Firstgas, Vector, Powerco). These companies recover the costs of their investments, plus a regulated rate of return, from gas users through charges levied on retailers, which are then passed on to consumers.

- End user gas bills recover the costs of gas production, transmission and distribution, plus retail margins.

- While not directly part of the ‘downstream’ market per se, the Government has announced a $200 million joint exploration fund to work with the private sector to discover new gas resources, which could have implications for infrastructure assets. In November 2025, the scope of the fund was broadened to include a range of investments that can accelerate or increase the volume of gas to market in the short-, medium- and long-run.

4.3. Historical investment drivers

- The initial development of the gas transmission and distribution networks was driven by the discovery and production of the large offshore Maui and onshore Kapuni gas fields in the Taranaki region. Maui began producing in 1979 and output and usage continued rising until the early 2000s following further offshore and onshore exploration resulting in more fields being developed.

- Subsequent investment was spurred by the expansion of the network to connect major industrial users, electricity generators, and residential consumers across the North Island. Methanex’s arrival, as a large anchor customer, also drove increased investment.

- On the back of increased supply and large industrial users, the gas transmission and distribution networks were built to their present size and form, serving a broader range of industrial, commercial and residential customers.

- Investment in infrastructure networks, at a high level, is driven by underlying economic and population dynamics. However, investment is also fundamentally limited by the availability of gas, under current and future policy settings. Recent supply reductions, limited exploration activity and New Zealand’s legislated net zero carbon emission goals raise significant questions about future gas infrastructure investment.

4.4. Community perceptions and expectations

- In a nationally representative survey undertaken by the Commission as part of consultation on the draft National Infrastructure Plan, 70% of New Zealanders (who use gas) reported that gas services meet or exceed their needs, while 30% reported it somewhat or consistently fails to meet their needs.

- In general, consumers appear to be concerned about prices and security of supply for both gas and electricity. Ensuring prices do not increase significantly was the most important factor for New Zealanders (87%) when considering the future of energy. Security of supply was also important (84%) to respondents.179

4.5. Current state of network

- The total value of gas transmission, distribution, and storage infrastructure in New Zealand was approximately $2.2 billion in 2024, which was roughly the same as the value in 2014.

- New Zealand’s gas transmission network, owned and operated by Firstgas, consists of 2,517km of high-pressure underground pipelines, compressor facilities and above-ground stations, including 123 offtake points across the North Island.

- Overall investment in the network was approximately $85 million in 2024. Over the past decade, average capital expenditure has been $96 million. From 2019 onwards there has been a downward trend in investment.

- Over the past decade, the average ratio of renewal expense to depreciation was 0.46, indicating that assets have deteriorated in condition over the last 10 years, or not been replaced on a like-for-like basis.180

- The distribution companies split networks across different areas of the North Island. Firstgas operates just under 5,000km of lower pressure distribution pipeline through Northland, Waikato, the Central Plateau area, Bay of Plenty, Gisborne and Kāpiti Coast. Vector covers the greater Auckland region with a 7,000km pipeline network. Powerco has a 6,300km pipeline network across Taranaki, Hawke’s Bay, Horowhenua and Manawatū, Porirua, Hutt Valley, and Wellington. The GasNet network consists of 413km of mains and 276km of service lines covering the five communities in the Whanganui region.

- Alongside the reticulated network, there are around 300,000 residential and commercial customers who are served by bottled LPG for cooking and water heating. Bottled LPG remains an important fuel source in the South Island, which lacks natural gas reticulation.

- The Commission publishes performance dashboards that can be used to understand changes in the performance of New Zealand’s energy sector over time.181

4.6. Forward Guidance for capital investment demand

Forecast investment levels for gas pipelines and storage

This table provides further detail on our Forward Guidance, which is summarised in Chapter 3. Further information on this analysis and the underlying modelling assumptions is provided in a supporting technical report.182

- The Commission’s Forward Guidance covers investment in the gas transmission and distribution networks, rather than upstream assets like production.183

- Our forecasts for the gas network are derived from modelling by the Climate Change Commission, which has created scenarios for meeting our net zero emissions targets. These scenarios include demand for gas, which we have converted to capital requirements.

- Based on Climate Change Commission scenarios, to meet our emissions targets gas demand will eventually be replaced by electricity and other sources. Revised production forecasts show supply is reducing faster and sooner than previously forecast.184 Current MBIE projections show production declining from about 120 PJs today to less than 40 PJs by 2035. Absent any new discoveries or greater production, this level would require significant reductions in industrial, commercial and residential demand and is only sufficient to meet current thermal electricity generation demand.

- Steady investment to maintain current pipeline assets will likely continue until the wave of new electricity generation, transmission, and distribution becomes available around 2040. At some point after this period, the existing network for natural gas is likely to be retired, though there is potential to repurpose some of the assets to deliver biofuels.

- This downward trend in investment, as well as the level, aligns closely with 2024 disclosures on future investment plans made by gas pipeline businesses to the Commerce Commission.

4.7. Current investment intentions

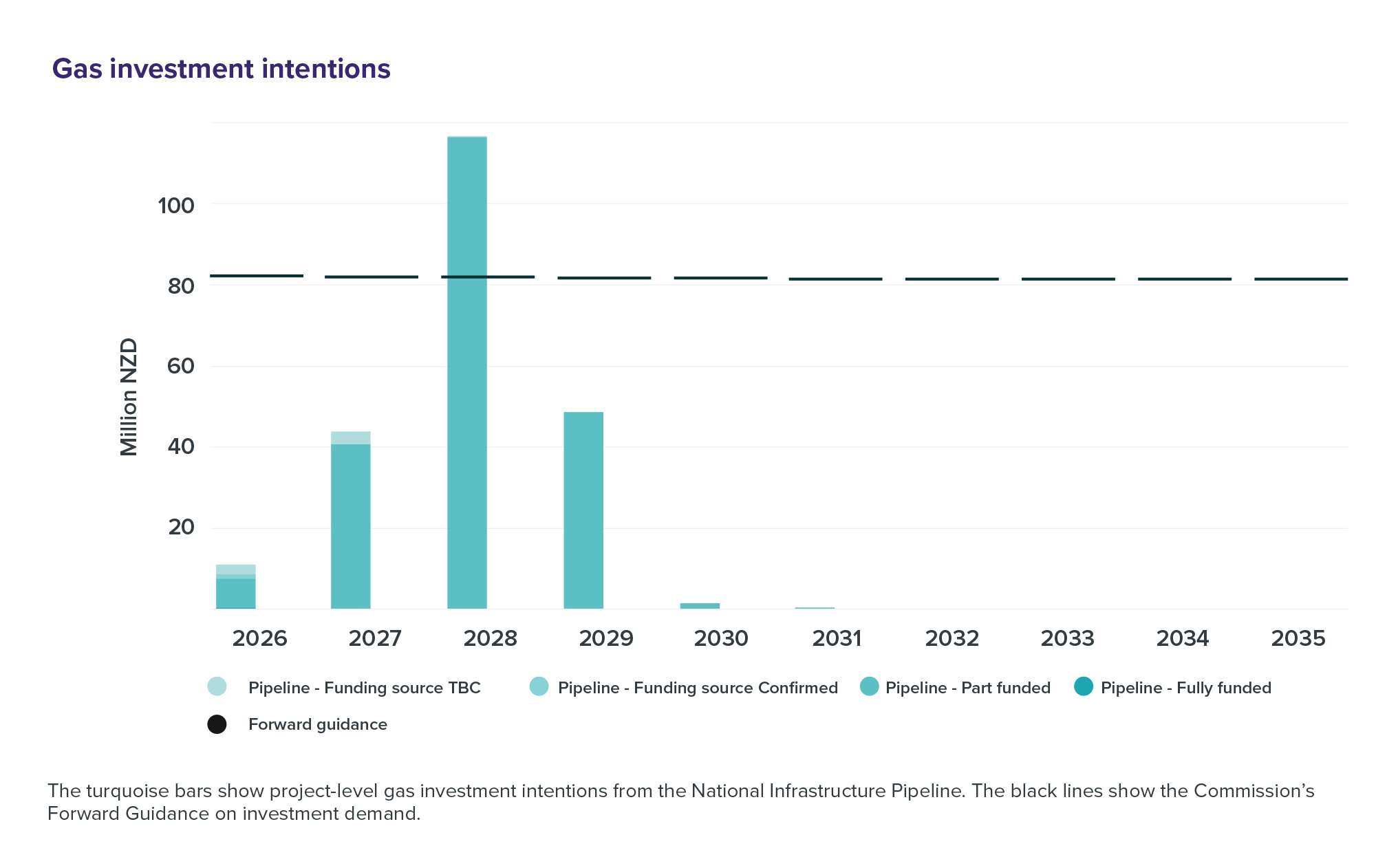

- The following chart shows projected spending to deliver initiatives in planning and delivery in the Pipeline (turquoise bars). The black lines show the Commission’s Forward Guidance for gas investment.

- The Commission currently collects only limited project data from gas transmission and distribution companies, so forward intentions in the Pipeline appear to be below the Commission’s forecasts for the next couple of years but catch up in 2028. Intentions do not extend much beyond 2030. The Commission is working to expand coverage of the gas network in the future.

Figure 49: Gas investment intentions

The turquoise bars show project-level gas investment intentions from the National Infrastructure Pipeline. The black lines show the Commission’s Forward Guidance on investment demand.

{kind=link}

4.8. Key issues and opportunities

- Future asset management: Gas production is projected by MBIE to decline dramatically over the coming decades, with projected supply in 2035 expected to be 84% lower than in 2015. This reduction may require steps to manage the transition for users. Steps and risks include:

- Better gas security-of-supply reporting will be important to help end users understand and manage downside supply risks.

- A range of demand and supply-side actions will be needed to manage the transition, balancing the need to accelerate fuel switching, while ensuring overall energy security is maintained during the transition. The Government has announced that it will run a competitive procurement process for an LNG import facility.

- Reduced demand response for the gas and electricity sectors. Large industrial users of gas have been able to reduce production during periods of very high wholesale electricity prices, freeing up gas for electricity generation. If these industrial users reduce production in line with declining gas supply, the electricity and gas systems may lose this additional level of demand response.

- In its 2023 default price path determination for gas transmission and distribution, the Commerce Commission approved shortening the assumed asset life of gas pipelines, allowing companies to recover depreciation expenses from users over a shorter period, which led to a small increase in customer bills. Over time, this and other network costs will need to be distributed over a smaller set of end users, which is likely to affect prices and affordability.

- Innovations in renewables: While traditional sources of natural gas are in decline and there is significant uncertainty around further exploration and future discoveries, renewable sources of gas are being explored. This includes producing biogas and converting it to biomethane and introducing the use of hydrogen blends to be transported across networks. There is not a clear view across network operators as to whether these alternatives are viable from a scaling perspective, and any potential switch to renewable sources may also trigger associated investment in network assets (for example, new lower pressure compressors) which may test existing price-quality paths.

- Policy certainty: Policy uncertainty may continue to have an impact on the outlook for future gas supply, including permitting for exploration and production from any new exploitable resources that are found, but also whether imported LNG is introduced as an electricity generation fuel. These uncertainties will influence investment decision making around future asset investment, including demand management practices and fuel switching – all of which will have an impact on prices. Large industrial users are particularly affected, as they are likely to face higher costs of switching to alternative fuel sources and longer required lead times for investment. Better gas security-of-supply reporting and stable and consistent transition planning can help to reduce investment uncertainty and disruption.