Content

Content

Waste and resource recovery

15.1. Institutional structure

Service delivery responsibilities

- Solid waste infrastructure and services are provided by both territorial local authorities and private firms. A three-tiered system exists where central government (Ministry for the Environment) sets national policy, and local and regional councils are responsible for planning, consenting, procurement and service provision – often in partnership with the private sector.

- Collection, recycling and disposal services are managed through council infrastructure and contracts or provided as a wholly private service. There are many different service arrangements and asset ownership models across New Zealand’s districts and regions for waste management and recycling services.

- Territorial authorities (councils) are also mandated by the Waste Minimisation Act 2008 to develop Waste Management and Minimisation Plans (WMMPs), which guide local service provision and infrastructure decisions.

Governance and oversight

- Multiple pieces of environmental legislation set the rules around the activities of this sector: the Resource Management Act 1991 (RMA), the Waste Minimisation Act 2008 (WMA), the Litter Act 1979, the Local Government Act 2002 (LGA) and the Climate Change Response Act 2002 (CCRA), which includes the Emissions Trading Scheme (ETS). These Acts are all administered by the Ministry for the Environment.

- National direction under the RMA includes a national environmental standard on air quality, requiring the flaring of methane from landfills, and a national environmental standard for soil contamination. The Government intends to replace the RMA with a Planning Act and a Natural Environment Act in 2026.

- The WMA provides for the waste disposal levy and waste minimisation fund, and promotes national strategy, with enabling powers for product stewardship schemes (for example, Tyrewise scheme) and product controls (used to ban single use plastic shopping bags and phase out hard-to-recycle plastics). While the WMA has played a key role in improving waste minimisation outcomes, the Government is currently working on amending the WMA to create a modernised and fit-for-purpose Act. This also includes repeal and replacement of the Litter Act 1979 into one piece of waste legislation.

- In 2024 national kerbside standardisation was introduced, requiring all territorial authorities to standardise the materials that they accept in council-managed kerbside recycling and organics.

15.2. Paying for investment

- Solid waste services are usually user pays – through a combination of council rates, one-off and subscription fees, and disposal levies – charged to those who create and dispose of waste.

- Central government applies a waste disposal levy for each tonne of waste deposited in most landfills. The Waste Minimisation Fund (WMF), sourced from waste levy revenue, provides contestable government funding to support projects by councils, businesses, and community groups that aim to reduce waste. A hypothecated portion of waste levy revenue is also provided to territorial authorities to support their waste minimisation services and infrastructure.

- Investment in waste and recycling infrastructure is funded through a combination of public and private sources. This includes council rates, user charges for waste services, revenue from the waste disposal levy and private sector investment. Key asset classes typically include landfills, collection vehicles, processing facilities and bin infrastructure. Investment decisions are driven by many factors, including commercial returns and markets, council contracts, WMF investment signals, and policy directions from both central and local government.

15.3. Historical investment drivers

- Early investment was primarily driven by public health requirements to dispose of refuse, leading to the establishment of local landfills with minimal environmental regulation.

- The introduction of the RMA significantly shifted investment towards engineered landfills with better environmental controls to manage effects, such as from leachate and landfill gas on land, water, and air quality.

- More recently, drivers have shifted towards resource recovery and sustainability, spurred by the Waste Minimisation Act 2008 and global shifts, such as China no longer accepting unprocessed recyclable materials that it used to accept.

- Policy settings can also impact investment directions and priorities, including how much waste needs to go to landfill, such as excavated soils during the construction and demolition process,219 and the treatment of landfill byproducts, such as biogenic methane. The latter is captured within the ETS, providing incentives to better manage and mitigate, such as harnessing the gas for power generation.

15.4. Community perceptions and expectations

This section summarises what we know about the New Zealand public’s perceptions and expectations of the waste and resource recovery sector, at a national level.

- Reducing the production of, and appropriately dealing with, waste is an important priority for New Zealanders.220

- Most New Zealanders agree we should produce less waste (85%) and are concerned about the impacts of waste on the environment (83%).221

- There is strong and growing public expectation for improved environmental outcomes, with high demand for accessible and effective recycling services and a desire to reduce waste sent to landfill.222

- In a nationally representative survey undertaken by the Commission as part of consultation on the draft National Infrastructure Plan, 72% of New Zealanders reported that rubbish and waste services are meeting or exceeding their needs, while 28% reported they are somewhat or consistently failing to meet their needs.

15.5. Current state of network

- New Zealand has 701 registered waste facilities which cover landfills, disposal facilities for organic material, and transfer stations. This includes 188 landfills, of which 41 are Class 1 municipal landfills.

- New Zealand produces the most municipal waste per capita in the OECD. However, definitions of municipal waste vary and more recent analysis with updated definitions has shown that New Zealand’s waste per capita may not be as high as previously reported.223

- Based on information from Stats NZ, we can infer that council-owned solid waste assets have a value of around $1 billion.224 However, many solid waste facilities are privately-owned, so the value of total waste assets is higher.

15.6. Forward Guidance for capital investment

- The Commission has not produced Forward Guidance for waste and resource recovery infrastructure.

- Future investment needs are likely to be driven by population growth, income growth and higher community expectations around environment standards.

- Maintenance of landfills will become more important and difficult as landfills become increasingly exposed to climate change and natural hazard events. For legacy waste facilities near coastal or river areas, erosion and runoff will need to be addressed with greater maintenance and investment.

- Future investment in landfills will also be linked to investment in other infrastructure sectors. For instance, landfill requirements will be affected by how wastewater capacity constraints are addressed.

15.7. Current investment intentions

- The data collected for current investment intentions is limited to local government entities in the National Infrstructure Pipeline. Specific reporting on capital spending for waste or resource recovery is not a required activity for inclusion in local government long-term plans.

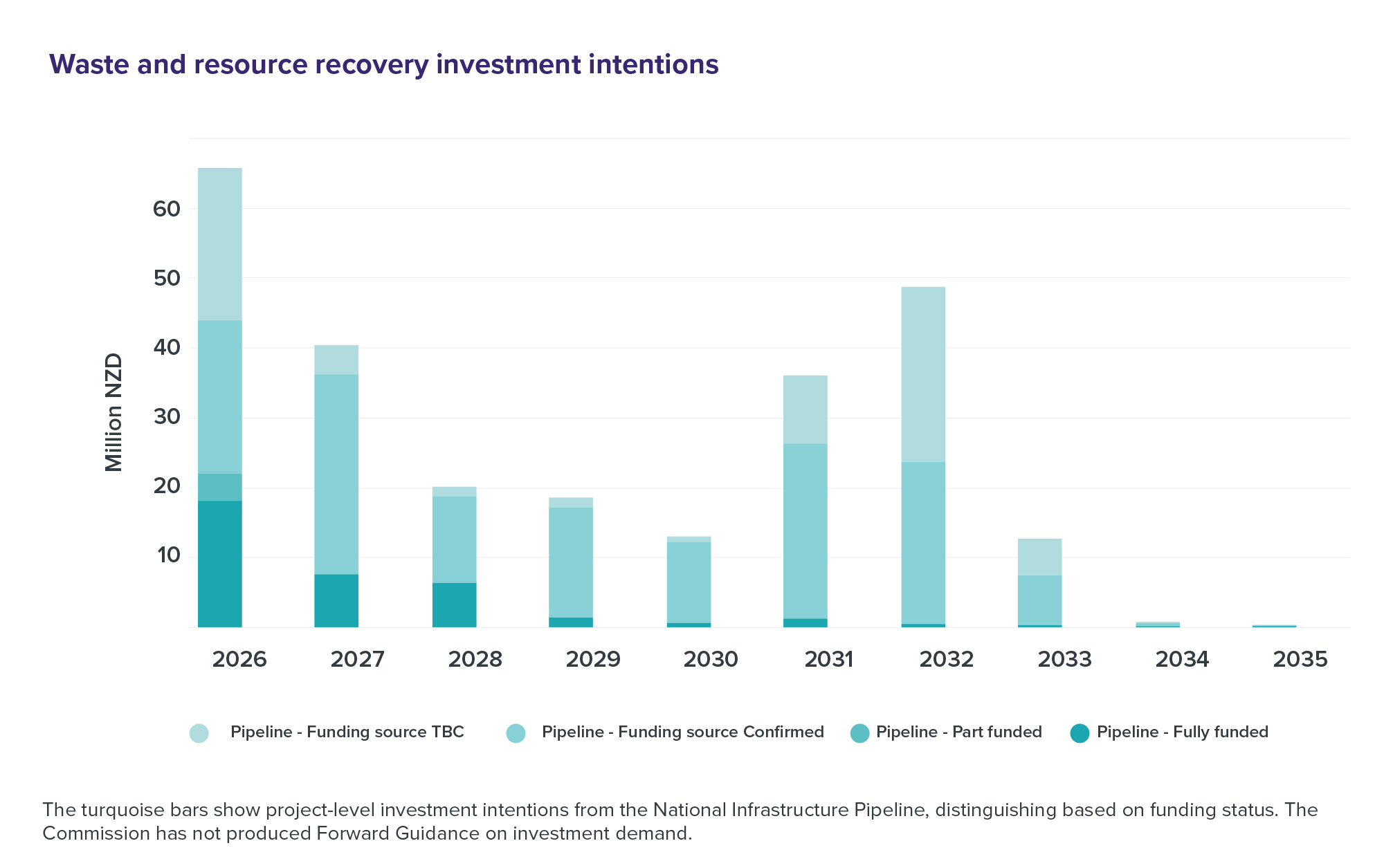

- Data from the Pipeline indicates that waste management accounts for 2–3% of the value of all projects reported by local government. Around 15% of future projects are currently fully funded.

Figure 60: Waste and resource recovery investment intentions

The turquoise bars show project-level investment intentions from the National Infrastructure Pipeline, distinguishing based on funding status. The Commission has not produced Forward Guidance on investment demand.

{kind=link}

15.8. Key issues and opportunities

- Coordination: Standardising kerbside collections nationwide has the potential to create economies of scale, improve the quality of recycled materials, boost public participation, and stimulate investment in domestic processing. This will be particularly important for urban areas and towns. Rural areas could also benefit from standardisation of accepted waste and recyclable materials, but may require financial support from local and central government to implement these programmes.

- Planning and engagement: Engagement with the commercial infrastructure waste sector should be undertaken to align infrastructure priorities and investment. There is also the opportunity to ensure that urban developments are planned to reduce waste and enable waste management servicing and capacity. Defining solid waste as infrastructure in resource management law may have benefit, particularly facilities such as district or regional resource recovery or waste disposal facilities.

- Optimising investment: Developing reliable and comprehensive national waste data is a major opportunity to inform evidence-based policymaking, infrastructure planning, and performance measurement. In addition, well-designed behaviour-change initiatives and information campaigns can help ensure that existing infrastructure is used efficiently, and new investment is being used as intended.

- Technology: Developing a view on the potential costs and benefits of opportunities for improved resource recovery, and more onshore recycling of materials like plastics, glass, tyres, and other materials, presents a possibility for creating economic value, generating jobs, and reducing New Zealand's environmental footprint.

- Pricing and revenue: For waste facilities funded by councils, rates affordability concerns will put funding pressure on investment and programmes. Better pricing of waste services could reduce possible funding gaps and help support greater minimisation of waste services and ensure greater equity across the system. Industry-led product stewardship schemes are also becoming an alternative form of user pays which could assist in funding future investment.