When stakeholders understand the direction of travel, planning becomes more efficient and delivery more effective - this is the essence of 'going slow to go fast'.WSP submission

Content

Content

4.1. Strengthening long-term asset management and investment planning

Te whakapakari i ngā whakahaere rawa tauroa me te whakamahere haumitanga

Context

Our Forward Guidance describes a sustainable level and mix of infrastructure investment to meet future demands, but it doesn’t determine funding levels. The biggest investment driver over the next 30 years is the need to replace or rebuild the infrastructure New Zealand already has, potentially taking up 60 cents in every dollar of capital spending. It is up to the Government of the day to allocate funding for many types of infrastructure through the annual Budget. This process, which divides up revenue collected from general taxes and other sources, must balance many competing spending demands within constraints driven by the need to maintain fiscal sustainability.

The Investment Management System (IMS) requires central government agencies to develop long-term investment intentions. Agencies are meant to signal future investments based on their strategic planning and asset management practices. The Treasury oversees the IMS, which is part of the Public Finance System. It comprises the policies, processes and requirements to support agencies to plan and deliver investments, as well as guidance on how they should be looking after their existing assets.

Parts of the system work well, but there is significant room for improvement. We reviewed how New Zealand performs against the International Monetary Fund’s Public Investment Management Assessment framework, a best-practice framework for assessing public sector investment and asset management.76 Central government can lift its capability to plan, fund, deliver, and manage infrastructure in three main areas. These relate to improving long-term investment planning, budgeting for maintenance, renewals, and resilience of existing infrastructure, and strengthening assurance for public investment and major projects (discussed in the next chapter).

The current approach to long-term investment planning is disjointed. The Government of the day forecasts how much money will be available in future years for new capital spending on infrastructure projects and other capital investment. The 2026 Budget Policy Statement, for example, indicated $3.5 billion would be available each year for four years.77 The Commission has reviewed long-term investment plans across several sectors, including health, defence, police, corrections and education. Collectively, these long-term plans indicate a requirement for significantly more than $5 billion of capital spending each year, not including potential Crown capital funding requests for transport and ICT investment. This materially exceeds the amounts forecast in the Budget Policy Statement.

This chronic misalignment between signalled investment and available funding means decision-makers routinely face difficult trade-offs. To be effective, long-term asset management and investment plans – which should outline what agencies think they need to look after and renew their existing infrastructure, as well as what improvements might be required in the future – need to be linked to funding and pricing decisions and consider different demand and funding scenarios.

Infrastructure delivery becomes harder without sufficient planning. Weak incentives for long-term planning and a process that forces difficult trade-offs mean decision-makers struggle to prioritise well. As a result, investments can reflect short-term imperatives rather than quality planning.

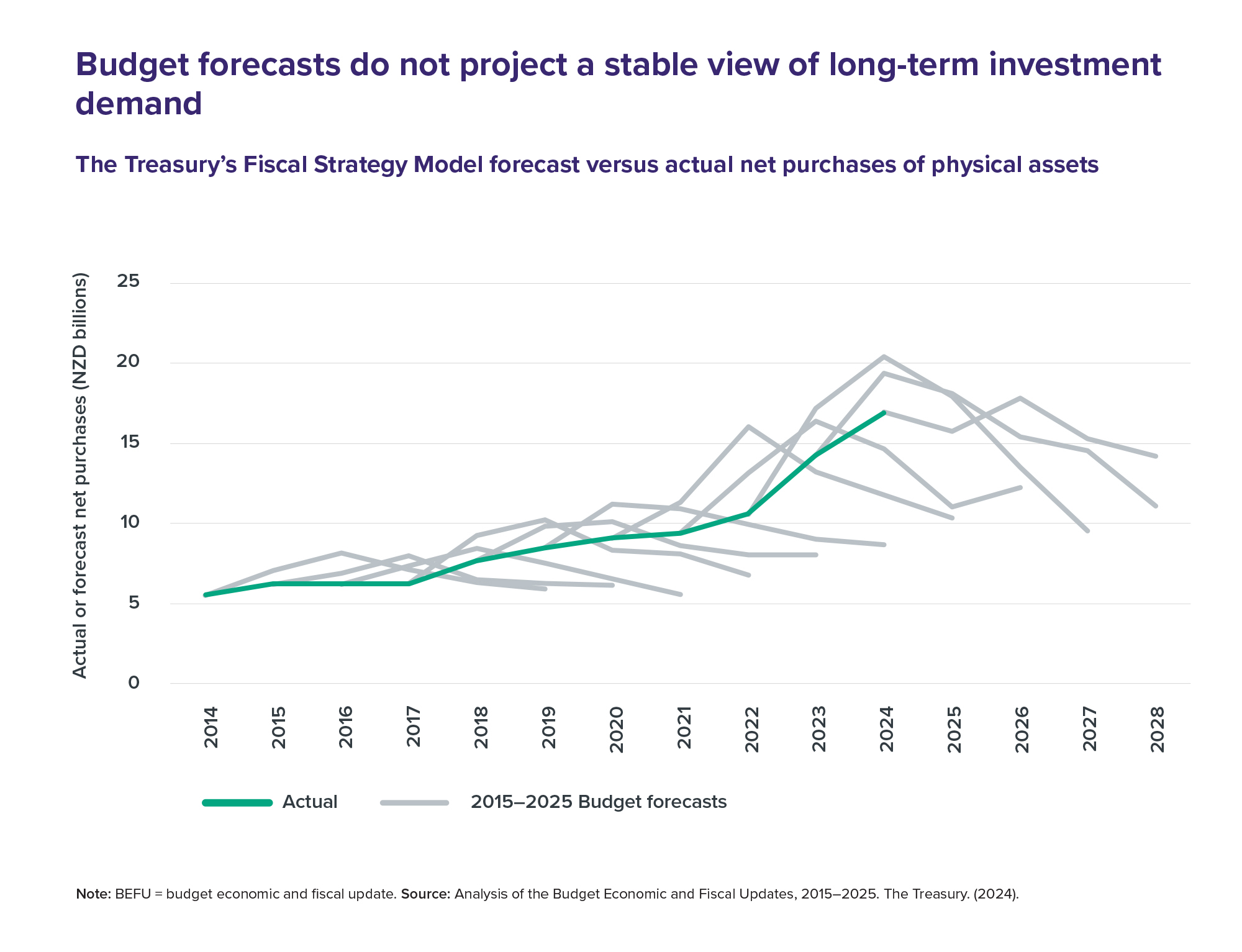

This means that investments often progress before they are ready. Budget forecasts consistently over-estimate capital investment in the short term and under-estimate it in the long term (Figure 25). This reflects optimism about how quickly newly funded (but immaturely planned) projects can be designed and delivered. For example, a review of 16 mental health units which received funding between 2015 and 2020 identified common issues in the planning phase, including a lack of detailed information and unrealistic expectations. This led to escalations, scope changes and delays.78

Better long-term planning supports a stable pipeline of work. The current mismatch between long-term investment intentions and available funding makes this difficult to achieve. Contractors need strong, credible future funding commitments to have the confidence to invest in equipment and workforce improvements. Swings in public infrastructure spending undermine confidence, which in turn makes project delivery more difficult and expensive. For New Zealand to be able to meet its infrastructure needs consistently and sustainably, the investment planning system needs to be improved.

Budget forecasts do not project a stable view of long-term investment demand

Figure 25: The Treasury’s Fiscal Strategy Model forecast versus actual net purchases of physical assets

Note: BEFU = budget economic and fiscal update. Source: Analysis of the Budget Economic and Fiscal Updates, 2015–2025. The Treasury. (2024).

{kind=link}

Strategic direction

Government agencies plan infrastructure investment with a clear view of long-term needs

Agencies should be required to develop long-term asset management and investment plans. These plans clarify what infrastructure owners need to do to maintain and renew existing assets to maximise their useful life for the lowest long-term cost. This eases fiscal pressures by deferring costly new investments until they are absolutely required. Plans should also assess what new investments might be required under various future scenarios to provide a comprehensive view of investment requirements.

Our Forward Guidance on future infrastructure demands is a start, but asset owners are best placed to do detailed long-term planning. The modelling in this Plan provides a broad view of the level and mix of investment demands that is likely to be affordable and needed in the long term. However, this is a high-level forecast. Capital-intensive central government agencies should be able to produce integrated long-term plans that provide a detailed view of their assets, as well as detailing current and future demands across their networks.

Data on long-term investment intentions should be consistent and complete. Agencies’ investment intentions are collected and reviewed by the Treasury on an annual basis. The Treasury provides Ministers with advice on these intentions through its Quarterly Investment Reporting, which is made public in a redacted form several months later. Information quality currently varies. Going forward, work is needed to standardise the level of detail provided by agencies, including clear communication of what service levels these investments are meant to support, and the risks associated with them.

Asset management and investment plans are credible and aligned with funding

Long-term asset management and investment plans should be credible, fundable and achievable within fiscal forecasts. While unconstrained plans can help reveal underlying investment pressures, they are of limited practical use if they significantly exceed available funding. Robust plans help to improve delivery confidence by giving the market greater certainty and allowing purposeful project sequencing. Agencies should identify the cost and timings of renewing existing infrastructure and the new investments required under different demand and funding scenarios, including an investment pathway consistent with our Forward Guidance. Asset owners also need to understand when funding is unlikely to be available so they can manage service delivery risks.

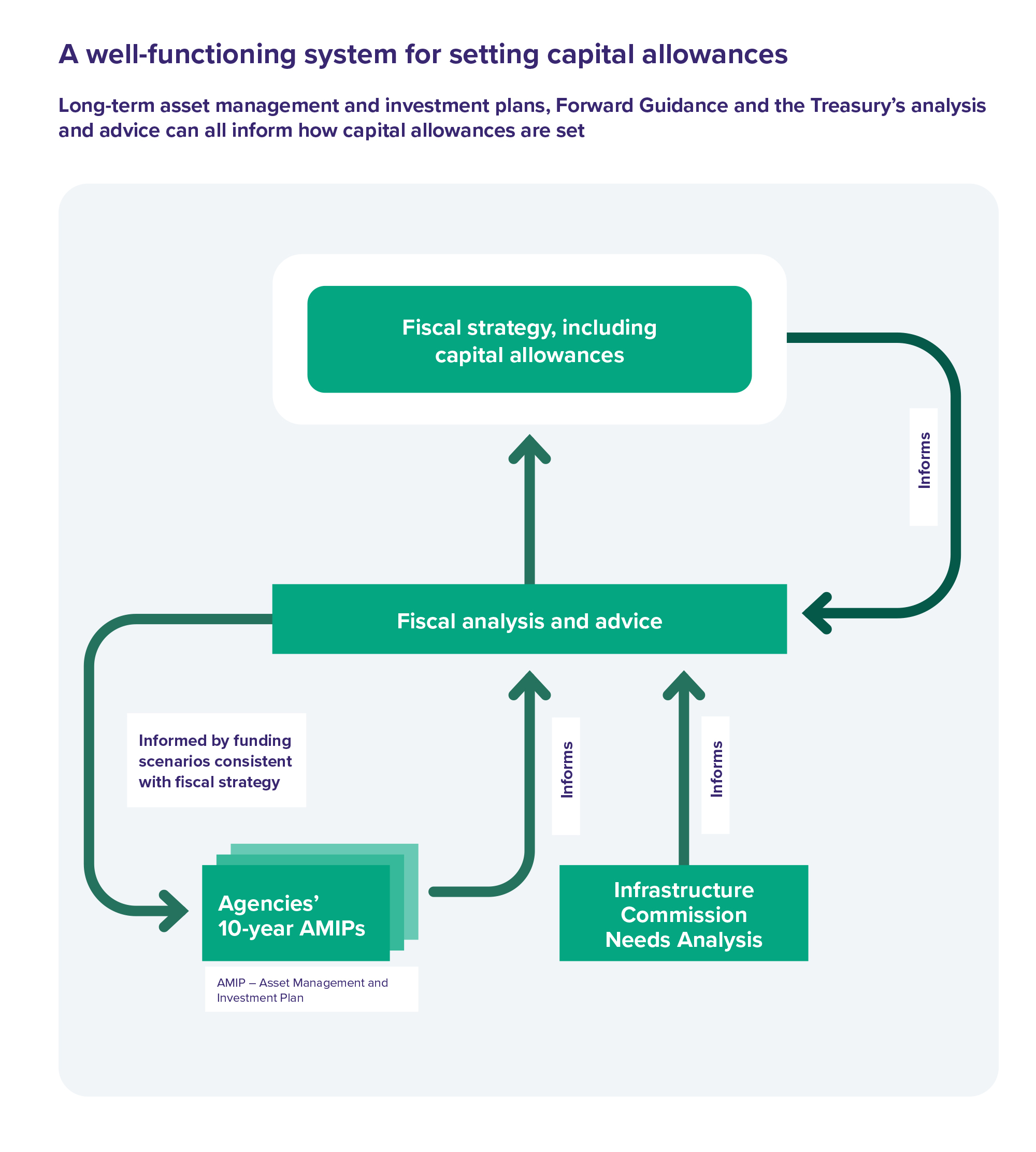

Changes are needed to address the systemic mismatch between investment planning and fiscal forecasting. Agencies should be required to include multiple investment scenarios in their plans, including at least one that is aligned with Government funding expectations for their sector and consistent with our Forward Guidance. Once long-term asset management and investment planning processes are sufficiently mature, the Government of the day could use these to help inform how it sets future capital allowances. Decision-makers can make prioritisation choices by relying on the Forward Guidance and its assessment of future needs for different sectors (Figure 26).

A well-functioning system for setting capital allowances

Figure 26: Long-term asset management and investment plans, Forward Guidance and the Treasury’s analysis and advice can all inform how capital allowances are set

{kind=link}

Budget decisions fund projects earmarked in long-term plans

Projects awarded funding through the Budget should have a link to long-term planning. Often this isn’t the case, which reinforces a short-term approach to planning and undermines the incentive for agencies to develop effective long-term plans. It also generates pressure to make detailed project announcements before planning has been completed, prematurely locking in a particular option.

When agencies do good asset management and investment planning, this should be reflected in Budget decision-making. Agencies should be expected to base Budget funding bids on projects previously identified in their asset management and investment plans. Bids should include well-developed business cases. This is important for ensuring that investment is coordinated and prioritised to areas of highest need.

Multi-year budgeting supported by good planning and monitoring practices could help. Once agencies have developed quality investment plans, the Government should start to plan its investment decision-making over a longer period than the next Budget. This could involve planning and signalling expected sectoral funding allocations or the likely sequencing of project funding decisions. In either case, any longer-term funding approach should be informed by and consistent with agency investment plans. Previous attempts to introduce multi-year funding had limited success due to other gaps in practices.

Getting it right will enable more effective procurement and delivery approaches. Providing more forward visibility over funding would enable agencies to establish efficient multi-year supply and procurement arrangements, strategically develop a more competitive supplier market, and smooth out their pipeline of work. This would then improve the construction sector’s ability to invest in the people and capabilities needed to deliver investment.

Asset owners plan carefully so they can handle unexpected changes

Uncertainty requires a sophisticated planning approach. Some trends are more predictable than others. For example, knowing we have an ageing population means we can prepare by building more hospitals. It’s harder to anticipate and prepare for things like the rapid uptake of artificial intelligence or sudden policy changes that affect demand for infrastructure, like migration levels. The cost of getting it wrong can be severe. Building too little infrastructure relative to demand can lead to congestion and poor service quality, at least until investment catches up. Building too much can result in assets that don’t cover their costs, creating ongoing financial burdens. Ongoing operating losses and maintenance make it harder to respond to other emerging needs.

It’s easier to respond when we have choices. When the trends driving demand for different types of infrastructure are uncertain or volatile, it makes sense to plan ahead and keep options open rather than making large, irreversible commitments that may not pay off. In the face of uncertain demand, little bets are safer than massive gambles.

Infrastructure providers can consider a broader set of future problems and opportunities in their planning. Rather than focusing on a small number of options for investment, they should think about how they would respond to different future scenarios. This is the approach that electricity generators take. They investigate more projects than they may seek to build in the near term to ensure they can respond to rising electricity demand when it occurs.

Providers can invest in land protection for infrastructure that may be needed in the future. This may mean buying land for future projects, obtaining designations for the use of land, or obtaining resource consents to enable future construction. Even when uncertainty exists about whether projects are needed, land protection can be valuable. It ensures that it is possible to build new infrastructure cost effectively when there is demand for it. Other actions, like futureproofing for infrastructure assets to be expanded if additional demand occurs, can also be useful.

Networks can be expanded bit by bit, as demand grows, rather than a ‘big bang’ approach that adds lots of capacity well in advance of demand. Large projects that are expected to take a long time to pay back are likely to be financially riskier than programmes of small projects. Pursuing them carefully, and selectively, is important when facing uncertainty.

![]()

Priority for the decade ahead

Manage assets on the downside

Forward Guidance: Our Forward Guidance highlights that demographics and factors like technological change will create challenges for all infrastructure networks. In education, for instance, we expect aggregate demand for school investment to moderate to 0.3% of GDP over the next 30 years due to the impacts of the ageing population.

What’s the problem?

While New Zealand’s population is all but certain to grow over the next 30 years, some regions, towns and even suburbs within otherwise fast-growing cities will have flat or declining populations. These areas face a unique challenge: remaining residents will end up paying more to maintain and eventually replace ageing infrastructure that was built to service a larger or growing population. As costs rise, more people may choose to leave, creating a vicious cycle that at its most extreme can lead to ‘ghost towns'.

Communities around New Zealand are already confronting this problem and some are opting to ‘pull back’ from some services to save money. In Southland and Gisborne, for example, councils are converting some paved rural roads back to gravel. Making these kinds of decisions is complicated by future uncertainty around population growth levels. In a low-growth scenario, as many as 45 territorial authorities will have stagnant or declining populations by 2053. Only one council will be in this position under a high-growth scenario.79

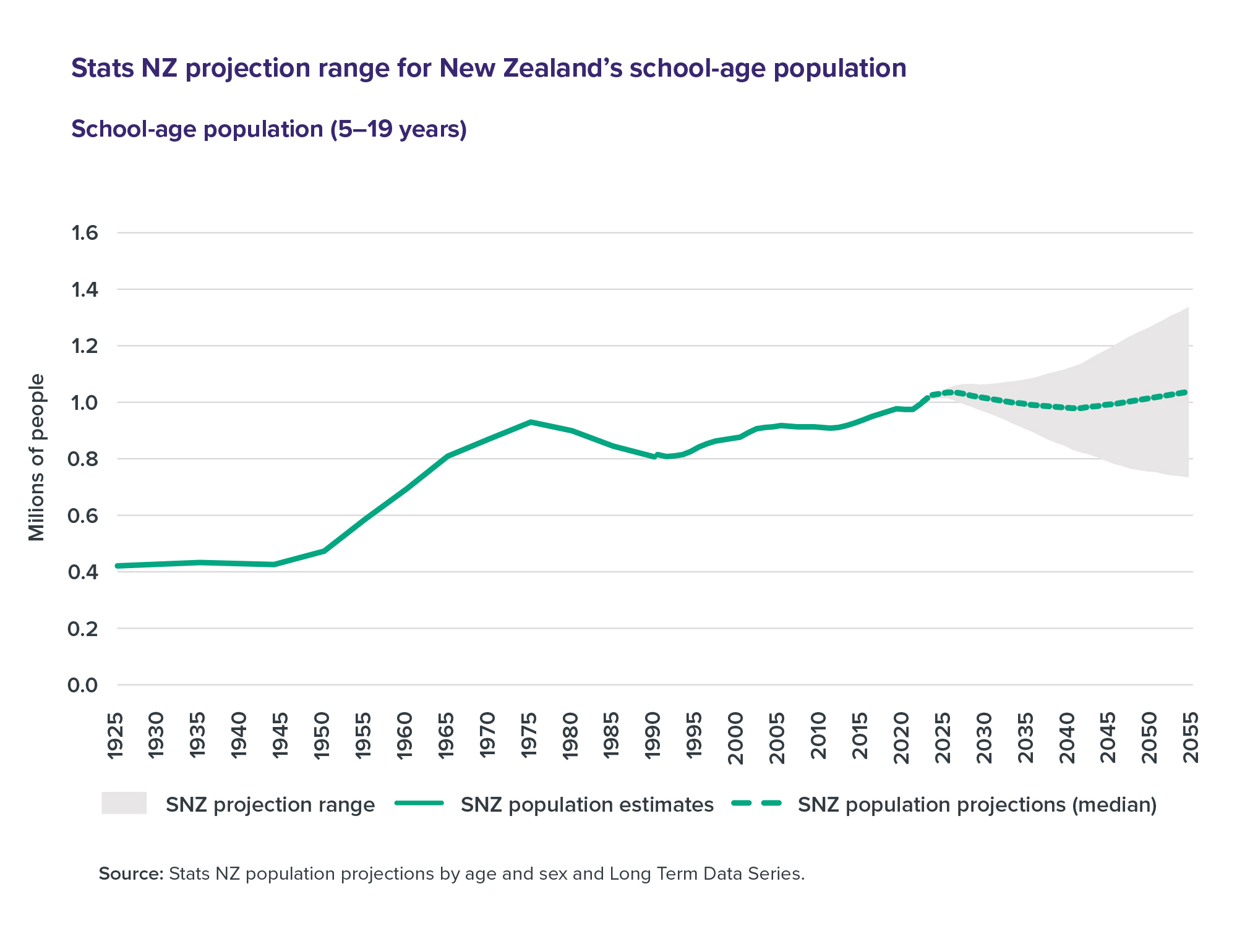

Managing declining demand is particularly important for education. After a long period of increasing student numbers, the overall school-age population is expected to be flat over the next 30 years, translating to less overall demand for schools (Figure 27). However, there will be local areas with growing student populations that will require investment. For example, almost 20% of schools (369) have capacity utilisation over 105%, while 11% (224) have utilisation of less than 50%. The challenge will be allocating scarce funding to spaces that are needed while right-sizing assets in declining areas to match demand.80 Otherwise, we risk an ever-growing, and potentially unaffordable number of classrooms.

It isn’t all about demographics. Faster internet speeds and disruption from the COVID-19 pandemic led to more people working from home, which reduced demand for transport services. Commercial infrastructure providers that need to make a profit have a strong incentive to respond when demand starts to weaken. In the gas sector, for example, gas distributors are considering how to right-size their networks due to declining gas reserves and customers switching fuels.

Figure 27: Stats NZ projection range for New Zealand’s school-age population

School-age population (5–19 years)

Source: Stats NZ population projections by age and sex and Long Term Data Series.

{kind=link}

Key actions

- Ensure slow-growing or declining communities don’t build ahead of demand. In some cases, they should ‘pull back’ service levels to improve affordability for remaining residents.

- Consider multiple future scenarios in long-term asset management and investment plans. Planning for different levels of growth, or no growth at all, is crucial to guide what investments might need to happen when. This also includes setting aside funds required for decommissioning assets when there is insufficient demand to maintain them.

- Consider asset recycling within networks. Infrastructure providers, particularly central and local government, should look for opportunities to optimise their portfolios and shift resources towards high-growth areas, while also ensuring equity of access.