Content

Content

3.3 Fixing land transport funding and investment

Te whakatika i ngā tahua tūnuku whenua me te haumitanga

Context

New Zealand spends more on land transport than any other type of infrastructure. Mature road and rail networks connect most parts of the country, supporting the smooth movement of people and freight that underpins a well-functioning economy. While these networks perform reasonably well against peer countries, some important gaps remain. Land transport infrastructure providers face limited external oversight and no economic regulation to protect consumers – which is unusual compared with network sectors where consumers can’t choose between multiple providers. Transport faces several challenges, such as rising congestion on urban road networks, rising carbon emissions, and high health impacts from air pollution and road crashes.54

Central government has established arm’s-length entities to provide and manage transport networks. NZ Transport Agency Waka Kotahi (NZTA) is a Crown entity that provides state highways and co-funds local roads and urban public transport services. NZTA also performs regulatory functions. KiwiRail is a state-owned enterprise which provides rail infrastructure and services. These arm’s-length entities were established to retain public ownership of assets while applying commercial discipline independent from day-to-day Ministerial control. They were also designed to be self-funding from user charges.

NZTA acts as both funder and deliverer of projects – combining functions previously kept separate. Between 1997 and 2008, one Crown entity (Transfund, renamed Land Transport NZ in 2004) was charged with administering transport funding and making investment decisions. Transit New Zealand was responsible for state highways and had to bid for funding alongside local road controlling authorities. Maintenance took precedence over new capital works, and only the highest-value projects were funded.55

The Government Policy Statement on Land Transport (GPS-LT) directs spending in the sector. Unlike other network providers that invest to meet demand, land transport investment is heavily influenced by the Government of the day’s objectives. The Minister of Transport determines funding ranges for expenditure categories through the GPS-LT, based on advice from the Ministry of Transport but without independent oversight. In recent years, Governments have also directed specific projects for delivery, leading providers to spend more than user revenues allow.

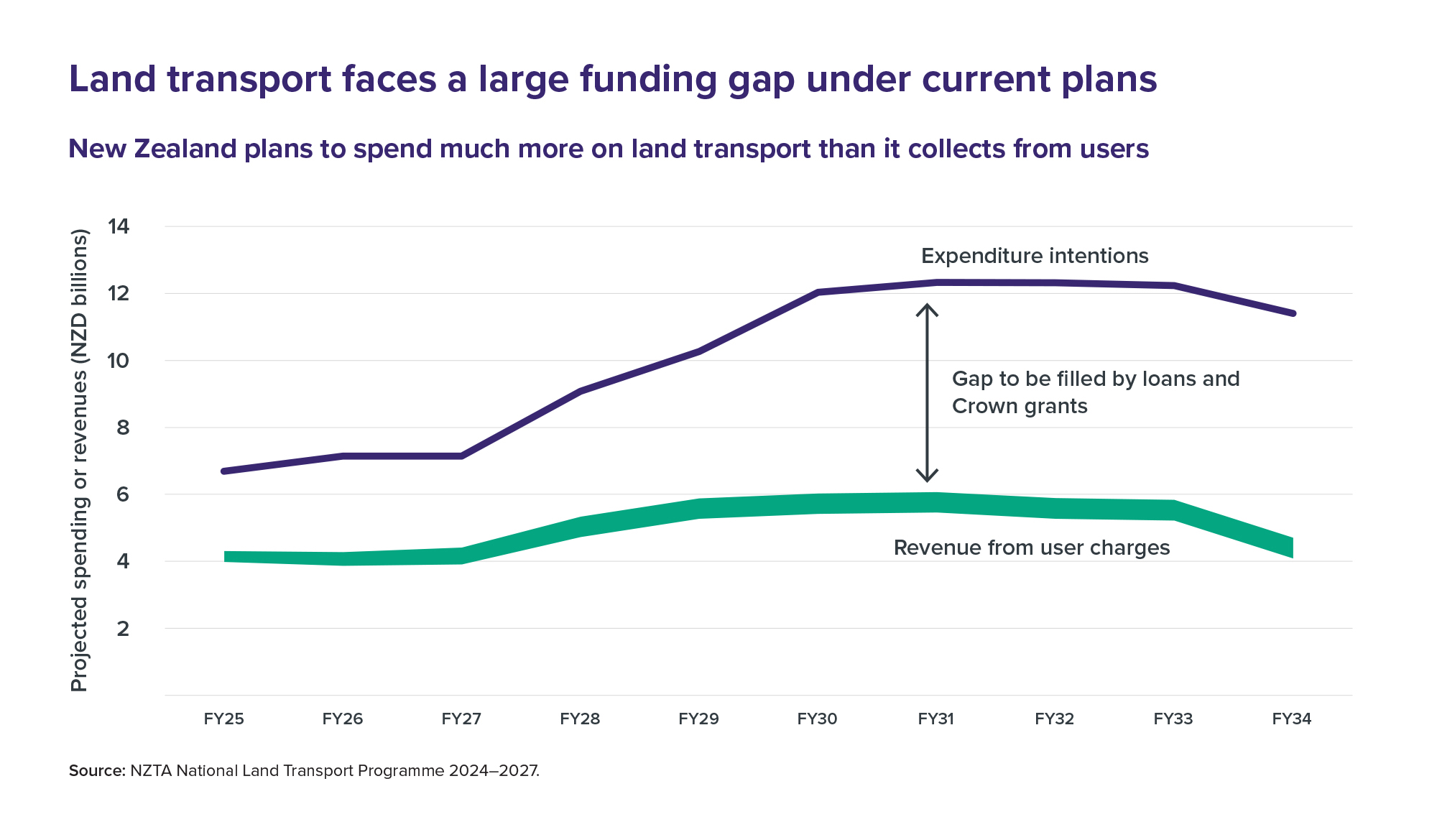

Historically, transport users funded almost all central government transport spending. This approach, which aligns with best practice pricing principles for network infrastructure, occurred mainly via fuel taxes and road user charges paid into the National Land Transport Fund (NLTF). Since the late 2010s, spending on roads and rail has far exceeded user revenues, requiring large top-ups from general taxes. In the 2024–2027 funding period, Crown grants and loans totalled $12.8 billion, or nearly 40% of the $32.9 billion in planned expenditure. These resources could otherwise support social infrastructure, and the funding gap is expected to persist (Figure 23).

At the same time, investment ambitions continue to grow. The National Infrastructure Pipeline includes around 25 major road, rail, and rapid transit schemes with a combined value over $100 billion – equivalent to more than 20 years of normal land transport revenue. Based on current estimates, delivering just the major roads programme in full over the next 20 years would cost $56 billion. Funding this entirely from petrol tax and road user charges would require a one-off 70% increase, equivalent to a 49 cent per litre increase in petrol tax.56 Further revenues would be required for the Waitematā Harbour crossing and major rapid transit schemes.

Household affordability pressures limit how much can be raised from users. Petrol costs and transport charges are consistently ranked in the top ten issues faced by households.57 Affordability concerns are likely to increase as the population ages and income growth slows. This reinforces the value of a more sustainable, demand-aligned investment approach in land transport – one that reflects what users can afford and what revenues can realistically support.

Land transport faces a large funding gap under current plans

Figure 23: New Zealand plans to spend much more on land transport than it collects from users

Source: NZTA National Land Transport Programme 2024–2027.

{kind=link}

Strategic direction

Transport investment matches the amount of money available from users

Return to a system funded predominantly by user charges. Doing so will give agencies like NZTA direct feedback on whether users are prepared to pay for investing in and operating land transport networks. There are some possible exceptions, including the ongoing use of rates to co-fund local roads and public and active transport, as well as cross-subsidies for public transport, active transport and rail initiatives that allow for more efficient use of existing networks. Crown funding can also play a role for emergency recovery events. In general, the funding model should shift to a state where Crown loans and grants aren’t required for land transport.

Investment should be made with greater independence. Our current transport spending ambitions present affordability challenges. To resolve these challenges, central government needs to be less prescriptive about how land transport funding should be allocated. Instead, transport providers should be accountable for selecting investments that maintain, renew and grow the network in line with user demands. Greater autonomy, coupled with independent oversight, can enhance commercial discipline, confine investment to available revenue and reduce network integration challenges. Borrowing should be used carefully, with appropriate accountability mechanisms in place.

Essential spending on renewals and maintenance should be prioritised first in budgeting. Each new road or railway needs to be maintained and renewed over its lifetime. If transport funding decisions are not sufficiently independent, funds for maintaining and renewing the network may need to be kept separate. Regular maintenance is more cost effective than sporadic maintenance, saving funds for other land transport priorities. Over the long-run, this approach will result in a higher-value approach to land transport investment.

Ongoing subsidies for rail require assessment. Central government has primary responsibility for funding below-rail assets, which currently run at a significant loss.58 The cost of maintenance, renewals and improvements is estimated at an average $500 million per year over the coming decade.59 While there may be a case for subsidising rail, doing so requires a demonstration that the benefits of investing in rail exceed those offered by other public infrastructure investment opportunities.60, 61

![]()

Priority for the decade ahead

Prioritise and sequence major land transport projects

Forward Guidance: Between 2010 and 2022, New Zealand spent around 1.3% of GDP per year on building and replacing land transport infrastructure, not including spending on maintaining and operating networks. Over the next 30 years, we expect this to moderate to around 1.0% per year as demand growth slows and investment rebalances toward renewals. That level of spending would fit within user revenues and allow existing networks to be maintained, renewed, and gradually improved. However, current investment ambitions go well beyond this level.

What’s the problem?

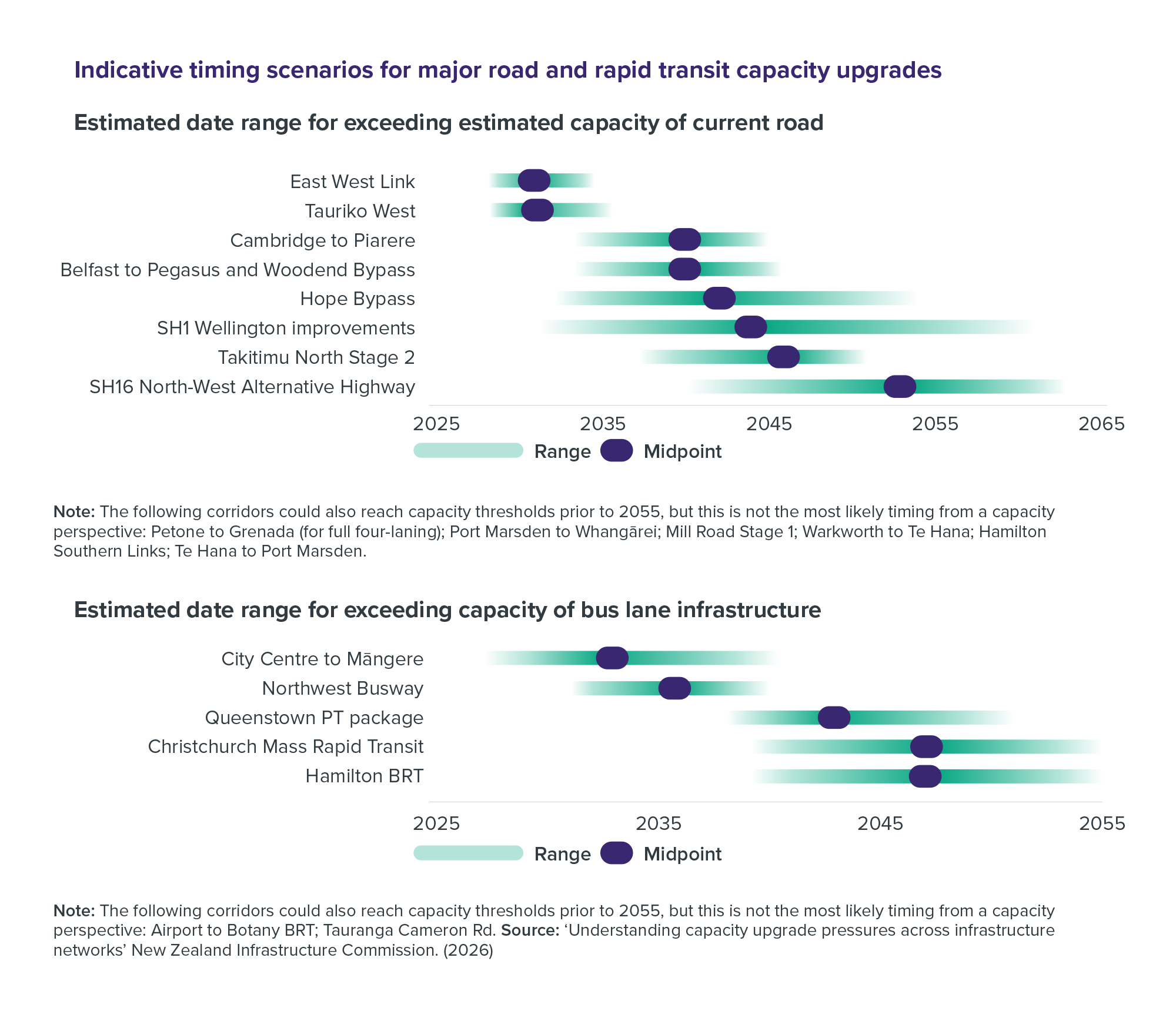

New Zealand’s major transport project pipeline has grown much faster than the funding available to deliver it. This includes plans for 17 Roads of National Significance (RoNS), major rapid transit projects such as Auckland’s Northwestern Busway, and a new Waitematā Harbour Crossing. Taken together, these ambitions far exceed the revenue likely to be available over coming decades.

Cost escalation compounds the problem. The RoNS projects are expected to cost significantly more per kilometre than earlier New Zealand motorway and expressway projects, and significantly more than the OECD average.62 Indicative target cost ranges published by NZTA suggest costs should ideally be much lower.63 The Northwestern Busway is expected to cost much more than previous New Zealand busways, potentially exceeding the per-kilometre cost of many underground rail projects overseas.64 These cost increases constrain what can be delivered without displacing other needs.

Decision-makers must align projects with demand, prioritise low-cost solutions before major upgrades, stage big builds over time, and protect funding for maintaining and operating existing networks. Our Forward Guidance predicts funding will be available for improvement projects, but not enough to build all major projects at once. An affordable programme must keep costs within benchmark ranges, align upgrades with demonstrated demand growth, and subject projects to rigorous cost-benefit analysis with independent assurance.

To illustrate what a demand-aligned approach could look like, the Commission has undertaken high-level analysis of demand growth scenarios for announced but currently unfunded major projects. This analysis distinguishes between capacity pressures and other drivers of intervention, such as safety, resilience, and reliability, which are often addressed through a single, high-cost upgrade. In many corridors, capacity constraints appear to be years away, and networks could continue to perform effectively with targeted safety treatments, resilience measures, operational improvements, or demand-management tools rather than immediate major expansion.

As an indicative benchmark, a well-designed two-lane road can carry around 2,600 to 3,000 vehicles per hour, depending on traffic mix, while a well-designed bus lane can move roughly 2,400 passengers per hour each direction.65, 66, 67, 68

Our timing estimates are presented as ranges to reflect uncertainty about local growth and the potential for non-capacity issues to trigger earlier interventions. Subject to cost-benefit analysis, projects in high-demand, high-growth corridors may warrant earlier consideration, while others can be deferred. In the interim, lower-cost, more targeted investments can be used to address specific safety, resilience, or performance issues.

In some cases, like SH1 Wellington improvements and Christchurch Mass Rapid Transit, there is a wide uncertainty range for when capacity constraints might be reached. This reflects underlying uncertainty about how rapidly demand will grow as well as choices about how to respond to capacity pressures when it is costly to upgrade capacity. Even where there is a narrower uncertainty range, like Tauriko West or the East West Link, upgrades could still be staged to optimise value.

Figure 24: Indicative timing scenarios for major road and rapid transit capacity upgrades, Estimated date range for exceeding estimated capacity of current road

{kind=link}

The Waitematā Harbour Crossing project is different. Unlike other road and rapid transit upgrades, it is unlikely to be fundable through normal transport revenues. Building the original bridge required a steep toll, equal to $9 in inflation-adjusted terms.69 The current crossing faces

maintenance, resilience, and capacity pressures, but repeated investigations have yet to identify an affordable solution.

New revenue will be needed to fund a new crossing. The Commission’s high-level analysis suggests that a $9 toll on both new and existing crossings could raise up to $7–9 billion, depending on the tolling period.70 Higher tolls may not raise more revenue, as they would divert too many users and erode viability, and tolling only the new crossing would sharply limit revenue. Other funding mechanisms are possible, but would likely require non-users to contribute funding which may not be considered equitable or favourable. Decision-makers will ultimately need to confirm revenue potential from tolling or other funding instruments like Infrastructure Funding and Financing Act levies, and identify options that fit within this envelope. In the meantime, time-of-use-charging, interim busway upgrades, and improved maintenance and monitoring should be considered to extend the life of the existing asset.

Key actions

- Use Forward Guidance to set realistic investment and revenue paths. This will help assess FED/RUC options and ensure long-term plans match sustainable revenue expectation.

- Prioritise low-cost, high-value improvements first. Use intervention hierarchies and demand-management tools like congestion pricing to address immediate issues while deferring expensive upgrades until genuinely needed.

- Align pricing and land-use policies. Ensure that zoning, development patterns and pricing tools support demand for major upgrades, rather than undermining their utilisation.

- Sequence major projects using value for money thresholds. Consider traffic volumes, public transport patronage, safety performance and cost benchmarking, supported by Infrastructure Priorities Programme assessments, to guide where and when major investment is justified.

- Develop new revenue tools where necessary. For projects that cannot proceed within existing funds, tolls, targeted levies, and other revenue mechanisms should be investigated, with budget envelopes reflecting the revenue these can credibly generate.

Revenues support an efficient level of investment in maintaining and improving networks

Revenue levels should reflect the cost of operating, maintaining, renewing and improving networks. There is currently no prescribed methodology for setting fuel taxes or road user charges, meaning charges can end up too high or too low.71 For example, the Government may hold user charges down during periods of high inflation even as the cost of operating the network rises. In recent years, revenue collected per kilometre travelled has been about 30% below the historical average despite elevated investment levels, reflecting short-term decisions to cut petrol taxes in response to inflation.72 Transport also generates wider costs, like air pollution and the health system impacts of road crashes, that are not currently factored into user charges, but could be considered as part of future revenue-setting approaches.

User charges also need to reflect users’ ability and willingness to pay. Charges may need to increase to overcome price freezes, which contributed to the NLTF’s inflation-adjusted purchasing power falling 21% since the last increase in FED and RUC.73 However, public feedback on the draft National Infrastructure Plan highlighted concern about further price increases. Low-income households spend a higher share of their after-tax income on transport.74 Moderating transport expenditure, while providing options for households to avoid the cost of owning and operating a private vehicle, would help affordability and address equity concerns.

Our Forward Guidance suggests capital spending on land transport should moderate from recent elevated levels. We forecast investment demand based on New Zealanders’ historical willingness to pay. Slowing population and income growth, alongside the potential for shifts in network usage as our economy decarbonises, suggest that land transport costs should represent a smaller share of household expenditure going forward. In this context, we would expect investment to shift away from state highway improvements toward maintenance, renewals, public transport, and resilience. Our Forward Guidance can inform decisions on funding levels and the user charges needed to support them.

Revenue decisions also require independent oversight. Other monopoly network service providers receive assurance and oversight in the form of economic regulation or audit. Given the significant implications on household costs, independent oversight of transport prices, through economic regulation or otherwise, could protect consumers while providing Ministers with confidence that the agreed revenue levels are both sufficient and reasonable.

Providers are efficient and accountable for delivery and asset management

New Zealand spent more on land transport between 2013 and 2022 than any other sector. The relative importance of the sector and its potential to displace spending in other areas means it should be subject to robust oversight and independent assurance over investment.

Infrastructure providers need to prioritise the highest value new projects. Higher spending on transport projects in recent years has coincided with a period of declining influence of cost-benefit analysis to inform project selection. Methodology changes make value for money assessments difficult to compare over time, but projects seemingly had to meet much higher thresholds in the 1990s and early 2000s. Land transport projects should be selected only where their benefits significantly exceed their cost. Investment decisions should be revisited as more information on costs and benefits comes to light.

Investment decisions require independent oversight. Investment assurance provides confidence that investments are strategically aligned, provide value for money and are deliverable. In other network infrastructure sectors, like electricity transmission and distribution, fixed-line broadband telecommunications, airports, and water and wastewater, performance-based economic regulation is used to lift efficiency and accountability.75 While land transport infrastructure has not historically been subject to economic regulation in New Zealand, international examples like the UK’s Office of Rail and Road illustrate that such an approach can be applied to ensure that transport expenditure promotes the long-term benefit of consumers.

![]()

Recommendation 2

Land transport funding and oversight

Reform the land transport funding and investment oversight system to ensure financial sustainability and enhance economic and social outcomes by aligning investment expectations with available revenue and strengthening efficiency and accountability in delivery.

Implementation pathway

This could be implemented by:

- Returning to a system where investment is confined to user revenues, with investment and borrowing decisions made at arm's length from Government.

- Establishing economic regulation or other independent oversight to ensure efficient investment and revenue levels that reflect cost.

- Embedding organisational structures and principles that prioritise funds for renewals and maintenance.

- Strengthening efficiency and accountability in delivery through independent assurance and clear performance expectations.

- Reviewing institutional structure, legislation and funding instruments to apply these principles effectively.

Responsible agencies

Ministry of Transport (lead), in consultation with New Zealand Transport Agency and other delivery entities

Timeframe

Complete public consultation on reform proposals within 24 months of the Government’s response to the National Infrastructure Plan.