Content

Content

Social housing

17.1. Institutional structure

Service delivery responsibilities

- Social housing is rental accommodation provided at below market rates, usually targeted and allocated to those with specific housing needs. Most social housing is funded by central government through the income-related rent subsidy (IRRS).

- The largest provider of social housing is Kāinga Ora – Homes and Communities (Kāinga Ora), a Crown entity. Kāinga Ora provides around 73,000 social housing tenancies, around 84% of all government-funded social housing places. Around 200,000 people live in Kāinga Ora homes, making it the largest landlord in New Zealand.

- Government-funded social housing is also provided by Community Housing Providers (CHPs), with 61 non-government entities providing around 14,000 government-funded social housing places. Some councils have also established independent CHPs to manage their social housing stock and access IRRS funding.

- In addition, sub-market rental accommodation is also provided by local councils and community organisations.

- Governments have also provided funding for housing interventions across the housing continuum, including emergency housing, transitional housing, affordable rentals and shared ownership schemes.

Governance and oversight

- The provision of social housing is regulated by the Public and Community Housing Management Act 1992, which is administered by the Ministry of Housing and Urban Development (HUD). CHPs are required to be registered with the Community Housing Regulatory Authority, which monitors CHPs to ensure they are well-governed, financially viable and delivering appropriate services to their tenants.

- In addition, the Residential Tenancies Act 1986 regulates social and non-social housing tenancies, including the rights and responsibilities of tenants and landlords, healthy home standards and disputes management.

- Kāinga Ora is a Crown entity with a board appointed by the Ministers of Housing and Finance. The Kāinga Ora board is the primary monitor of Kāinga Ora management and is accountable to the responsible Ministers for the performance of the organisation. HUD also monitors Kāinga Ora, advises Ministers on the performance of Kāinga Ora and acts as the responsible Ministers’ agent.

- To access government-funded social housing, individuals must apply to the Ministry of Social Development (MSD) to be added to the Housing Register, with eligibility based on age, residence, income and asset tests. MSD assesses the housing need of applicants and assigns a priority rating and score using the Social Allocation System. As suitable social housing places become available, Kāinga Ora and CHPs offer tenancies to shortlisted applicants from the Housing Register. As of November 2025, there were roughly 19,500 households on the Housing Register.

17.2. Paying for investment

- Government-funded social housing is funded mainly from user charges (below market rate rents paid by tenants) and subsidies paid for through general taxation. Government funding for social housing is provided through ongoing payments for services, rather than up-front grants. The primary payment is the IRRS. Access to this subsidy requires that the rent charged to the social housing tenant is capped at 25% of their income, with the IRRS payment to the provider making up the difference between rent from the tenant and the rent the property would achieve on the private rental market. In addition, a supplementary payment called Operating Supplement (OS) is paid for newly built social housing places, to help cover the cost of financing construction.

- To pay for the upfront cost of building a social housing place, social housing providers need to borrow against their future cash flows of IRRS and OS funding. Kāinga Ora is required to borrow directly from the Crown, via New Zealand Debt Management (NZDM), at a small premium to the borrowing costs of NZDM.

- Social housing is purchased by HUD from CHPs primarily through 25-year capacity contracts, which are intended to provide CHPs with greater certainty over future cashflows. CHPs borrow to fund construction costs from financial institutions, including banks and the Community Housing Funding Agency (CHFA). The Government has recently taken decisions to make it easier and cheaper for CHPs to borrow, by providing a loan guarantee scheme to participating banks and a liquidity facility to the CHFA.

17.3. Historical investment drivers

- Investment in social housing is driven by a combination of population growth, overall housing need and differing Government policy approaches. Investment in social housing has occurred in several waves, as different Governments have responded to community need for housing.

- The first wave of significant investment in social housing was in the 1930s prior to the Second World War. Investment remained elevated during the 1940s and 1950s but gradually started falling through the 1960s. There were also waves in the late 1970s and late 1980s.

- Investment in social housing was relatively low from the 1990s, including a period where the total social housing stock was falling due to asset sales. This was part of a wider reform to housing supports, with greater emphasis placed on direct financial support to households. Transfers of social housing from government to non-government ownership was a focus in the 2010s, with limited additional investment.

- The most recent wave of social housing investment started around 2018. This was driven by a significant increase in demand for social housing, with the number of applicants on the Housing Register more than quadrupling between 2017 and 2022. Need for a range of housing supports increased over this period, leading to the use of motel accommodation for emergency housing and investment in transitional housing.

- Current social housing investment is also driven by the need to renew Kāinga Ora homes that are reaching the end of their useful life, exacerbated by limited renewals and maintenance in previous decades. Waves of investment during the 20th century have become waves of renewal need in the 21st century.

17.4. Community perceptions and expectations

There is limited recent data available on the general New Zealand public’s perceptions, expectations and preferences for social housing.

- Public perceptions of the wider housing market are relevant, as social housing is one way of addressing wider housing affordability challenges. A range of studies show that addressing housing supply, affordability, and quality issues are consistently very important priorities for New Zealanders. For example:

- Housing, and the price of housing, was the top issue (alongside inflation/cost of living) selected by New Zealanders, averaged across 24 survey waves over seven years.228

- New Zealand’s supply of new housing was rated as poor/very poor by 67% of respondents and identified as the top infrastructure priority for New Zealand in a 2024 survey (of the options provided), with 55% of respondents selecting it.229

- In another survey, housing affordability was identified as the third top issue that the government should take action on, averaged across three years (2023–2025).230

- Housing affordability was the fourth most important priority, and cities not keeping up with growth was also very important for most New Zealanders responding to the Commission’s Aotearoa 2050 survey of over 23,000 people.231

17.5. Current state of network

- As of November 2025, New Zealand had roughly 87,000 government-funded social housing places, around 73,000 owned by Kāinga Ora and 14,000 owned by CHPs. In addition, non-IRRS social housing is also provided by local councils, Māori housing providers and other non-governmental organisations.

- Kāinga Ora had property assets, excluding land, of $17 billion in 2025. According to Stats NZ, the value of social housing stock owned by local councils, excluding land, was $4.5 billion in 2022.

- Investment in social housing as a share of GDP peaked in the 20 years after the Second World War (roughly 1-2% of GDP each year) with further waves of investment in the 1970s and 1980s. Since 1990, we’ve spent about 0.2% of GDP on building or renewing social housing each year. However, in recent years, investment in social housing has been elevated, with around 20,000 new social housing places being added since 2017.

- Since 1960, the ratio of investment to depreciation in social housing has been 121% , the lowest ratio of any horizontal or vertical infrastructure class according to Stats NZ data. This pattern likely reflects historical reductions in the total stock of social housing, the average age of stock increasing and potentially indicates a decline in the average condition of the stock originally built in the post-war period. The recent wave of investment has likely been reversing this trend.

- According to the OECD, about 3.8% of New Zealand’s housing stock is social housing, below the OECD average of 7%. New Zealand has 14.4 social houses per 1,000 people, which is below the OECD average of 32.7.232

- New Zealand appears to rely more on providing rent supplements, such as the Accommodation Supplement, rather than relying on constructing social housing. The OECD estimates that New Zealand spends just over 0.4% of GDP per year on rent supplements, which is sixth highest in the OECD.

17.6. Forward Guidance for capital investment demand

Forward Guidance for social housing

This table provides further detail on our Forward Guidance, which is summarised in Chapter 3. Further information on this analysis and the underlying modelling assumptions is provided in a supporting technical report.

- The Commission’s Forward Guidance assumes that the government will own and operate social housing in the same way it has in the last 10 to 20 years. It does not make assumptions about asset sales or the shift in ownership/subsidy models.

- The Commission projects that to meet the needs of a growing population, renewal requirements, and to catch up on years of underinvestment in renewals, investment over the next 30 years will need to be higher than it has been in the latest decade.

- Ongoing renewal requirements plus growth in construction costs alone will require about 0.16% of GDP (over $645 million in 2025) a year on average, before accounting for any growth in demand from a growing population or the need to catch up on deferred renewals.

17.7. Current investment intentions

- As the largest provider in the sector, Kāinga Ora’s Reset Plan, released in February 2025, provides insight into investment intentions for the sector.234 While exact decisions on capital investment are dependent on Ministerial and Board-level decisions, the Reset Plan sets out potential scenarios for investment. The Reset Plan’s central scenario projects between 1,500 and 2,000 new builds per year out till 2029, offset by demolitions and sales.

- In addition to Kāinga Ora’s investment, CHPs were funded to provide 1,500 social housing places in Budget 2024 and 550 social housing places in Budget 2025, with additional investment to be delivered through a Flexible Fund.

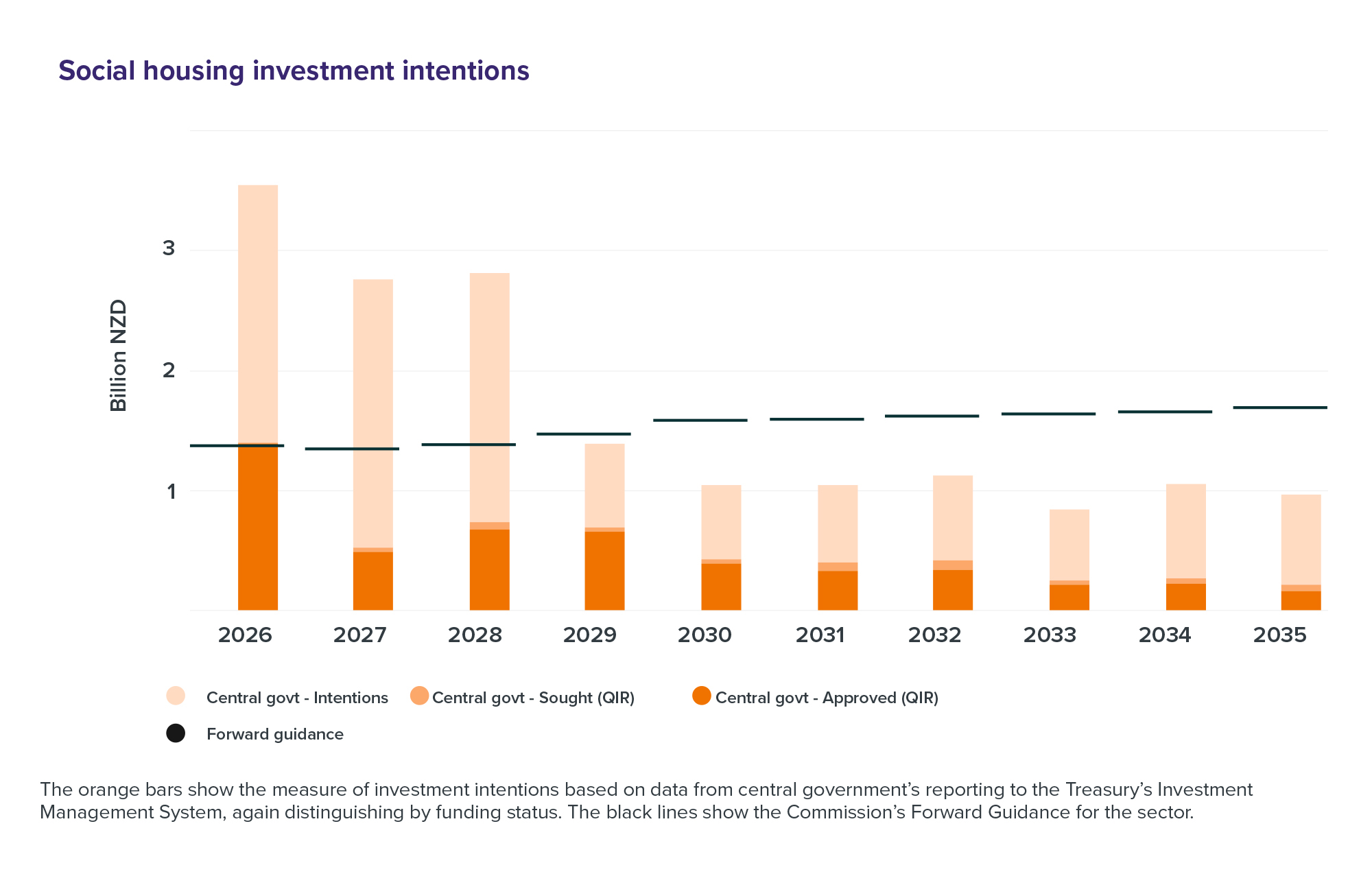

- The chart below represents planned and intended net investment in social housing activities (this is the cost of investment, less sales of assets). The Pipeline value is not used as a comparison in this chart as it only reports on asset creation and maintenance and so does not represent the net value.

Figure 61: Social housing investment intentions

The orange bars show the measure of investment intentions based on data from central government’s reporting to the Treasury’s Investment Management System, again distinguishing by funding status. The black lines show the Commission’s Forward Guidance for the sector.

{kind=link}

17.8. Key issues and opportunities

- Government’s approach to social housing: There are different views on the extent to which housing need should be addressed by government-provided social housing, non-government provided social housing, or direct financial assistance to households (such as the Accommodation Supplement). The choice of which approach to use will have a significant impact on required investment in social housing.

- Management of the asset portfolio: According to Treasury’s latest Investment Statement, the asset base of Kāinga Ora ($48 billion) is one of the largest in the Crown’s social portfolio.235 Given significant renewal requirements and continued elevated housing need, ensuring strong balance sheet and asset management is critical to meeting housing need. For example, use of asset recycling, selling houses that are less needed to build houses in higher need areas and typologies, helps to better meet housing need while reducing pressure on government capital allowances.

- Meeting housing demand: The types of social housing people need is changing over time. For example, over half of the applicants on the Housing Register are single adults who require a one-bedroom home, whereas less than 15% of Kāinga Ora housing stock, the majority of which was built decades ago, is one-bedroom units. In addition, social housing need is unevenly distributed across the country, being higher in small centres in the upper North Island, such as Rotorua, Gisborne and Whakātane, and lower in the South Island.236 Shifting to a housing stock that matches the needs of those on the Housing Register will require significant shifts in investment and asset recycling of houses in lower need areas and lower demand typologies. The Kāinga Ora Reset Plan and the new Housing Investment Strategy are responding to this shift in demand.

- Asset management: Low investment and renewal of government-owned social housing has been a significant issue over multiple decades, leading to significant renewal requirements over the next 15 years. Between 1990 and 2015, there was lower investment in government social housing, resulting in ageing and lower quality housing stock.237 There were likely many drivers for this, including funding restraints, land-use restrictions preventing intensification, and changes in how Governments view their role in social housing. Since 2015, significant investment in new social housing stock, supported by more enabling land-use settings such as the Auckland Unitary Plan, has increased average quality but significant renewal needs remain. The Kāinga Ora Reset Plan sets out scenarios to renew, refurbish and maintain assets at a moderate and sustained level over time.